Despite a challenging past four months, with several market disruptions and external pressures, Horizon’s team remains committed to steering the Fund towards its long-term goals. Today, the Horizon team is pleased to present an updated fund overview for mid-September.

Due to the reported disruption caused by the shutdown of a critical vendor at the end of May, the Fund was forced to pause new equity admissions throughout June, July, and August. Additionally, the Fund’s senior financing lender has paused all cash advances back to the Fund, while also requiring proceeds received from mortgage payoffs to be used to pay down their line. Due to these restrictions, the Fund’s daily operations and cash flows have been impacted, limiting its ability to purchase any new loans during this time period. As a result, the Fund’s portfolio has decreased in size, with 40 loans being repaid since June 30th. Also, since the senior financing partner is requiring all proceeds to be used to pay down their line, the Fund has also seen its leveraged capital decrease by ~$4.6M in this same timeframe.

In an effort to return the Fund to normal operations, the Investment Committee made the decision to reopen the Fund for new equity admittances on September 1st. In September, the Fund raised over $800K of new equity. No new loans have yet been purchased, however, as the Fund continues to receive additional equity, its Investment Committee will review opportunities to begin purchasing new loans. Horizon’s team is also continuing to work very closely with its senior financing partner and we are hopeful to return all operations back to normal in the coming months.

Below is a monthly breakdown of the Fund’s total equity, loan balances, and leveraged capital.

Portfolio Composition & Risk Management

When looking at portfolio composition and risk management for Horizon, a few of the main portfolio metrics the Horizon team considers are geographic location, weighted average leverage metrics, and project type. We underwrite and monitor these different metrics to ensure we are maintaining a balanced portfolio that aligns with our overall investment strategies.

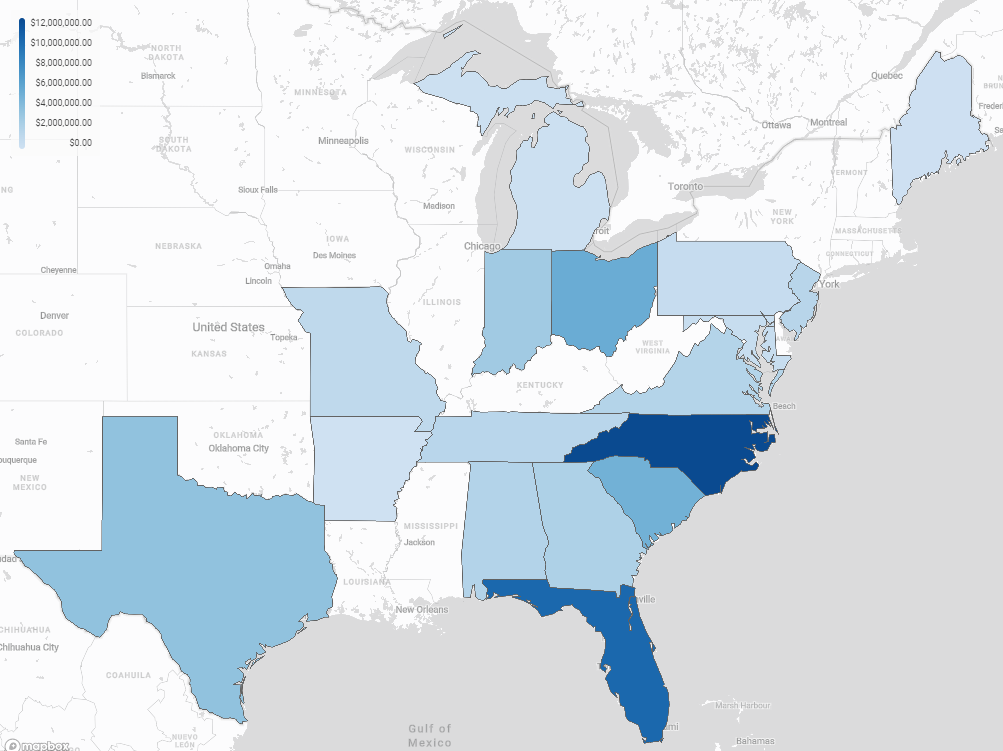

At the end of Q2, the portfolio's top markets were North Carolina (18.84%), Florida (18.66%), and Ohio (14.25%). Below you will find visuals to display Horizon’s full state concentration by gross loan amount, as of 9/16/2024. As no new loans have been purchased to date in 24Q3, recent geographic shifts in the portfolio are strictly due to recent loan repayments. While the top markets in the portfolio have remained the same, you will notice that North Carolina’s total concentration has shifted above 20%. As over a third of the loans held in North Carolina are over 95% complete on construction, we anticipate seeing a downward shift in the state’s total concentration as these loans repay in the coming months.

Horizon State Exposure – % of Total Portfolio as of 9/16/2024

| North Carolina. . . . . . 22.54% | Georgia . . . . . . . . . . . . 4.34% |

| Florida. . . . . . . . . . . . . 18.93% | Alabama. . . . . . . . . . . 3.80% |

| Ohio. . . . . . . . . . . . . . .10.20% | Virginia .. . . . . . . . . . . . 3.71% |

| South Carolina. . . . . . . 9.51% | New Jersey . . . . . . . . .3.33% |

| Texas . . . . . . . . . . . . . . 6.99% | Other . . . . . . . . . . . . . .10.67% |

| Indiana . . . . . . . . . . . . . 5.54% |

Horizon’s loan leverage metrics are also a vital piece to the portfolio’s overall health. These leverage ratios are what protect each loan against any potential downside risk. Below is a breakdown of each metric:

- Loan to As-Is Value (LTAIV): We have set a maximum LTAIV constraint per loan of 70%, and are targeting a portfolio below 65% LTAIV.

- Loan to Cost (LTC): We have set a maximum LTC constraint for any loan within the portfolio at 90%, while targeting a weighted portfolio makeup below 85%.

- Loan to After Repair Value (LTARV): The Horizon team has set a 70% maximum LTARV constraint for each loan and for the entire portfolio.

In the below table, Horizon’s month-over-month changes in WAVG loan leverage metrics are presented. All three portfolio metrics have remained at or below their target mark through mid-September.

Additional Horizon Portfolio Composition

Project Type – % of Total Book (9/16/2024)

Loan Performance & Delinquencies

Delinquency management is a core focus at Upright, beginning with rigorous underwriting practices and supported by our Servicing and Asset Management teams, who employ industry-leading strategies for effective recovery. These strategies include relationship-based borrower management, timely issuance of Notices of Default, and loss mitigation evaluations after 61 days of delinquency. Given the short-term nature of our asset class, understanding delinquency rates is crucial, as performing loans typically repay within 10 months on average, while delinquent loans may require longer resolution periods.

At the end of 24Q2, the Fund saw an uptick in its delinquency rate, moving to ~11%. As we have progressed through Q3, the Fund has continued to see increases in its overall delinquency rate, shifting from ~12% at the end of July to ~26% in mid-September. This uptick in delinquency, however, is not solely indicative of deteriorating loan performance. With continued restrictions from the Fund’s senior financing facility, the Fund’s loan portfolio has continued to be reduced in size, shrinking from a peak of 212 loans in the second quarter to a current portfolio size of 157. The Fund’s increase in delinquencies reflects the maturity of the loan book, as delinquency typically occurs in the later stages of a loan's term when initial interest reserves have been exhausted and projects encounter more complexities as they work towards repayment.

Throughout 24Q3, our Servicing team has worked proactively to address delinquencies. In July, the team managed 19 loans in the 31-90 day delinquency buckets, with Notices of Default issued promptly for loans exceeding 60 days delinquent. Despite efforts, the number of delinquent loans increased slightly in August, where 14 new loans entered the 31-60 day delinquency bucket. However, this trend has decreased slightly in September as only 6 new loans entered the 31-60 bucket.

Separate from the uptick in 31-60 day delinquencies, the Fund currently holds 13 loans in the 61-90 day bucket, 18 loans 91+ days delinquent, and three loans actively working through foreclosure. Our Asset Management team continues to explore foreclosure and workout options for all 91+ delinquencies, ensuring that we pursue the best possible outcomes. Additionally, of the 34 delinquent loans in the 61+ bucket, 19 are held between three unique developers. Of these 19 loans, 15 are more than 92% complete and we feel strongly that the developers will soon be able to exit these loans as the properties are listed for sale.

Below is a chart displaying the Fund's delinquency rates from June 2024 through mid-September 2024, presenting both the total count and the percentage of the active book based on the Unpaid Principal Balance of delinquent loans. This detailed transparency reflects our commitment to rigorous reporting standards and aligns with the MBA’s approach, while also providing an expanded view of our delinquency performance.

Horizon Residential Income Fund I, LLC

Thank you for your continued trust and support in Horizon Residential Income Fund I, LLC. We welcome all questions and suggestions and look forward to a successful and rewarding journey together.

Sincerely,

Matthew Rodak

Chief Executive Officer