This is an ongoing thread of updates on the service interruption with one of our payment processing partners. We will continue to update this page as we learn more and make progress toward unlocking transactions and investments.

July 2026 Update

Dear Investors,

Below is an update as to where things stand with overall return of capital in the various Upright investment products. We appreciate your patience and will continue to provide updates here as needed.

PFNF

This week we will be initiating a PFNF principal distribution for $200K, which represents ~2.63% of the remaining PFNF note balance. We’ve now returned 89.46% of all PFNF principal since we began this distribution plan.

We do expect the remaining loans to resolve at a slower and perhaps more sporadic pace. While we remain diligent in our efforts to bring the portfolio to a final resolution, many of the remaining loans are working their way through court or legal proceedings, most of which we’re beholden to the timeline of the applicable legal system.

We will continue to endeavor to make a distribution each month to the extent liquidity is created on the underlying portfolio. Otherwise, our go-forward disbursements and corresponding updates will shift to an interval that aligns with liquidity availability of the portfolio.

Since the last report, we have had a total of 4 loans repay. We also continue to run parallel disposition strategies (i.e. loan sales, bulk REO sales, workouts, etc.) on the portfolio where and when it makes sense.

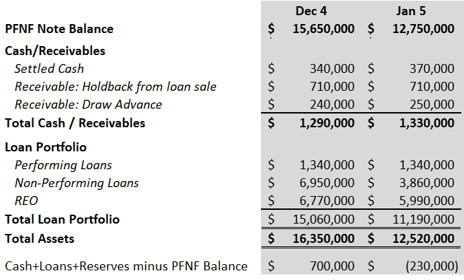

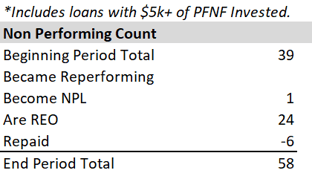

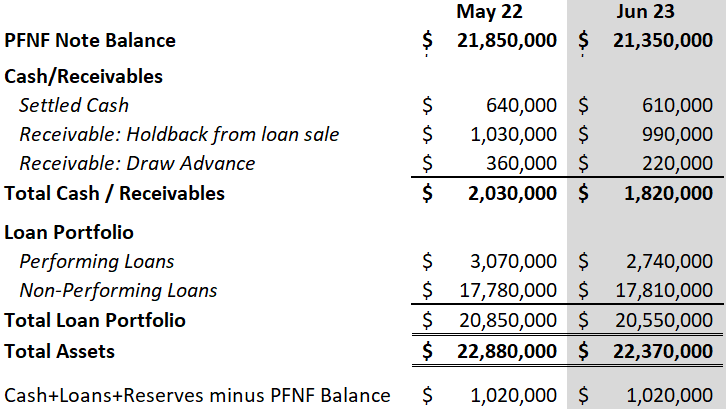

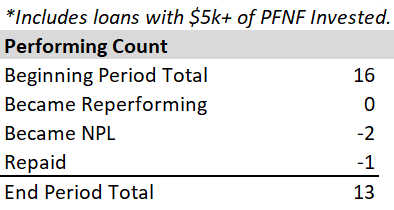

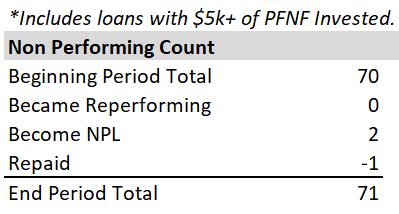

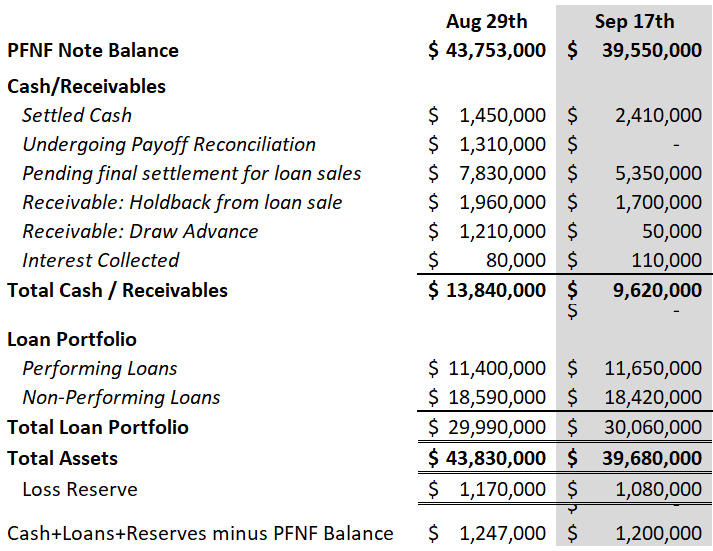

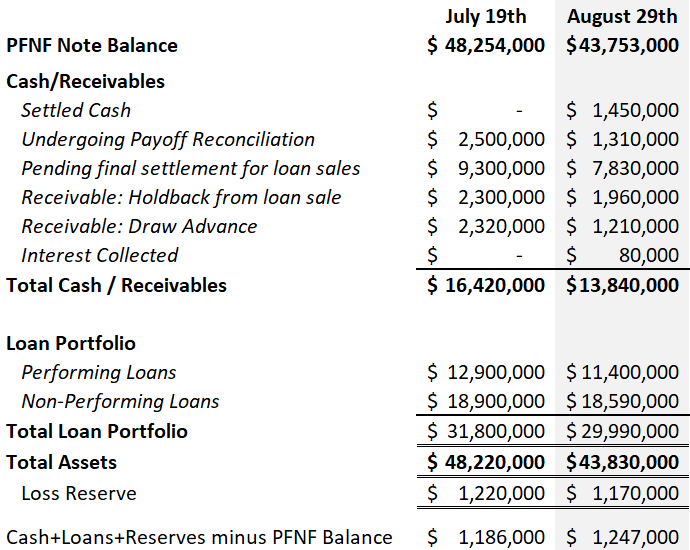

The below is a current snapshot of where remaining PFNF funds are allocated relative to last time this was reported.

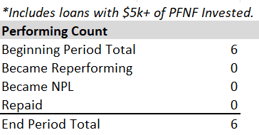

We started the period with 30 loans with 14 now being in REO status. We received payoffs for 4 loans this period.

Please note that some loans are “portfolio” loans, meaning that they have more than one underlying property securing the loan. As the individual properties are sold/repaid, the portfolio loan remains “open” while liquidity is generated on the “partial release” of the underlying properties. This may skew the unit count numbers until all of the underlying properties of the portfolio loan are repaid and the loan is “closed”. The below tables show the movement of loan counts for the period.

Managing this portfolio and expediting loan repayments remains a high priority. We will continue to push forward on bringing this portfolio to a resolution.

Please consider the components of this analysis are incredibly dynamic as payoffs, loan sales, servicing advances and various reconciliation efforts are ongoing daily.

Borrower Dependent Notes (BDNs)

Since the last report, 6 BDN loans have been repaid, representing $1.4M of principal. To the extent that an underlying loan is making interest payments, we continue to process interest distributions 2-3 business days after they are received. If you have not received an interest payment on one of your BDN investments, this is because the underlying loan has not made its interest payment. Our team continues to reach out to past due borrowers and work them through our asset management and loss mitigation process.

We continue to strive to provide detailed updates on all individual BDN investments while balancing the time spent on updates relative to focusing that time towards creating positive outcomes. We’ll continue to strive to provide additional updates on these investments and keep the information updated best we can. Please know that even if an update hasn’t been posted, we’re monitoring and working each loan towards a resolution.

RBNF

There has not been any meaningful liquidity on the underlying RBNF portfolio since the last report. The balance of RBNF notes is $1.19M. The remaining balance is largely REO or late stage foreclosure. We continue to work on resolving the underlying loans to create liquidity for distributions on these notes.

Horizon

We continue to generate liquidity on the Horizon portfolio and a monthly distribution will be processed within the next week. We continue to be committed to managing the Horizon portfolio and maximizing the outcome for Horizon investors.

We appreciate your patience as we work to return capital to investors. We remain committed and optimistic that liquidity will continue to be created on the remaining portfolio. We ask that you continue to trust that we’re doing all that we can to get these resolved as quickly as practicable while trying to optimize the total return of capital.

Matt and The Upright Team

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

June 9th, 2026

PFNF

This week we will be initiating a PFNF principal distribution for $950K, which represents ~11.11% of the remaining PFNF note balance. We’ve now returned 89.18% of all PFNF principal since we began this distribution plan.

The portfolio continues to make progress through the foreclosure to REO and final disposition process. Since the last report, we have had a total of 5 loans repay. We also continue to run parallel disposition strategies (i.e. loan sales, bulk REO sales, workouts, etc.) on the portfolio where and when it makes sense. We remain optimistic that liquidity will continue to be created on the underlying assets in the coming month.

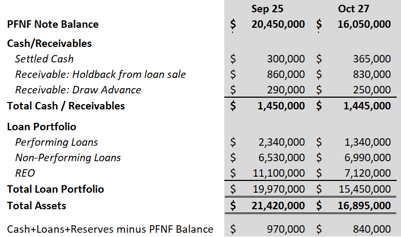

The below is a current snapshot of where remaining PFNF funds are allocated relative to last time this was reported.

The overall loan portfolio decreased by ~$970k since the last report. We unfortunately experienced some principal loss on the grouping of repaid loans this period. While this is disappointing, we also have some REO properties that we think may be sold for more than our principal balance to help offset some of this loss. We remain committed to maximizing the total return of principal on this portfolio while also working towards providing liquidity as quickly as possible.

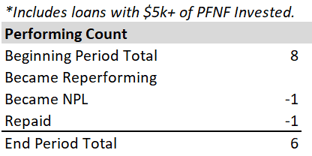

We started the period with 1 performing and 34 non-performing loans, 15 of which are now REO. One performing and 4 non-performing/REO loans repaid this period.

Please note that some loans are “portfolio” loans, meaning that they have more than one underlying property securing the loan. As the individual properties are sold/repaid, the portfolio loan remains “open” while liquidity is generated on the “partial release” of the underlying properties. This may skew the unit count numbers until all of the underlying properties of the portfolio loan are repaid and the loan is “closed”. The below tables show the movement of loan counts for the period.

Managing this portfolio and expediting loan repayments remains a high priority. We will continue to push forward on bringing this portfolio to a resolution.

Please consider the components of this analysis are incredibly dynamic as payoffs, loan sales, servicing advances and various reconciliation efforts are ongoing daily.

Borrower Dependent Notes (BDNs)

Since the last report, 9 BDN loans have been repaid, representing $3.5M of principal. To the extent that an underlying loan is making interest payments, we continue to process interest distributions 2-3 business days after they are received. If you have not received an interest payment on one of your BDN investments, this is because the underlying loan has not made its interest payment. Our team continues to reach out to past due borrowers and work them through our asset management and loss mitigation process.

We continue to strive to provide detailed updates on all individual BDN investments while balancing the time spent on updates relative to focusing that time towards creating positive outcomes. We’ll continue to strive to provide additional updates on these investments and keep the information updated best we can. Please know that even if an update hasn’t been posted, we’re monitoring and working each loan towards a resolution.

RBNF

There has not been any meaningful liquidity on the underlying RBNF portfolio since the last report. The balance of RBNF notes is $1.19M. The remaining balance is largely REO or late stage foreclosure. We continue to work on resolving the underlying loans to create liquidity for distributions on these notes.

Horizon

We continue to generate liquidity on the Horizon portfolio and a monthly distribution was processed at the end of last week. We continue to be committed to managing the Horizon portfolio and maximizing the outcome for Horizon investors.

We appreciate your patience as we work to return capital to investors. We remain committed and optimistic that liquidity will continue to be created on the remaining portfolio. We ask that you continue to trust that we’re doing all that we can to get these resolved as quickly as practicable while trying to optimize the total return of capital.

Matt and The Upright Team

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

May 5th, 2026

PFNF

This week we will be initiating a PFNF principal distribution for $850K, which represents ~9.04% of the remaining PFNF note balance. We’ve now returned 87.83% of all PFNF principal since we began this distribution plan.

The portfolio continues to make progress through the foreclosure to REO and final disposition process. Since the last report, we have had a total of 8 loans repay and are expecting another 6-10 to resolve in the next 30-45 days. We also continue to run parallel disposition strategies (i.e. loan sales, bulk REO sales, workouts, etc.) on the portfolio where and when it makes sense. We remain optimistic that liquidity will continue to be created on the underlying assets in the coming month.

The below is a current snapshot of where remaining PFNF funds are allocated relative to last time this was reported.

The overall loan portfolio decreased by ~$1M since the last report. We unfortunately experienced some principal loss on the grouping of repaid loans this period. While this is disappointing, we also have some REO properties that we think may be sold for more than our principal balance to help offset some of this loss. We remain committed to maximizing the total return of principal on this portfolio while also working towards providing liquidity as quickly as possible.

We started the period with 2 performing and 41 non-performing loans, 16 of which are now REO. We had no performing loans become non-performing. One performing and 7 non-performing/REO loans repaid this period.

Please note that some loans are “portfolio” loans, meaning that they have more than one underlying property securing the loan. As the individual properties are sold/repaid, the portfolio loan remains “open” while liquidity is generated on the “partial release” of the underlying properties. This may skew the unit count numbers until all of the underlying properties of the portfolio loan are repaid and the loan is “closed”. The below tables show the movement of loan counts for the period.

Managing this portfolio and expediting loan repayments remains a high priority. We will continue to push forward on bringing this portfolio to a resolution.

Please consider the components of this analysis are incredibly dynamic as payoffs, loan sales, servicing advances and various reconciliation efforts are ongoing daily.

Borrower Dependent Notes (BDNs)

Since the last report, 10 BDN loans have been repaid, representing $2.2M of principal. To the extent that an underlying loan is making interest payments, we continue to process interest distributions 2-3 business days after they are received. If you have not received an interest payment on one of your BDN investments, this is because the underlying loan has not made its interest payment. Our team continues to reach out to past due borrowers and work them through our asset management and loss mitigation process.

We continue to strive to provide detailed and timely updates on all individual BDN investments while balancing the time spent on updates relative to focusing that time towards creating positive outcomes. We’ll continue to strive to provide additional updates on these investments and keep the information updated best we can. Please know that even if an update hasn’t been posted, we’re monitoring and working each loan towards a resolution.

RBNF

There has not been any meaningful liquidity on the underlying RBNF portfolio since the last report. The balance of RBNF notes is $1.25M. The remaining balance is largely REO or late stage foreclosure. We continue to work on resolving the underlying loans to create liquidity for distributions on these notes.

Horizon

We continue to generate liquidity on the Horizon portfolio and expect to process another monthly distribution this week. We continue to be committed to managing the Horizon portfolio and maximizing the outcome for Horizon investors.

We appreciate your patience as we work to return capital to investors. We remain committed and optimistic that liquidity will continue to be created on the remaining portfolio. We ask that you continue to trust that we’re doing all that we can to get these resolved as quickly as practicable while trying to optimize the total return of capital.

Matt and The Upright Team

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

April 1st, 2026

PFNF

This week we will be initiating a PFNF principal distribution for $600K, which represents ~6.00% of the remaining PFNF note balance. We’ve now returned 86.62% of all PFNF principal since we began this distribution plan.

The portfolio continues to make progress through the foreclosure to REO and final disposition process. Since the last report, we have had a total of 9 loans repay and are expecting another 6-10 to resolve in the next 30-45 days. We also continue to run parallel disposition strategies (i.e. loan sales, bulk REO sales, workouts, etc.) on the portfolio where and when it makes sense. We remain optimistic that liquidity will continue to be created on the underlying assets in the coming months.

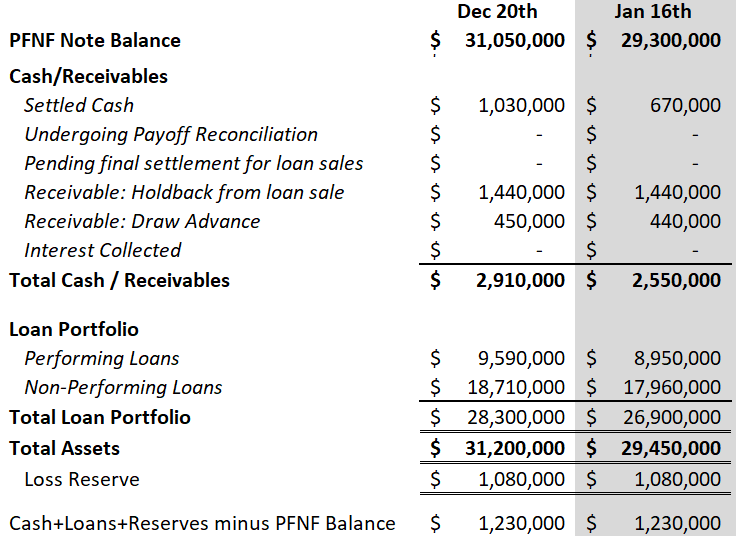

The below is a current snapshot of where remaining PFNF funds are allocated relative to last time this was reported. Please note that the below figures are inclusive of the $1.5M distribution that was processed on March 6th.

The overall loan portfolio decreased by ~$2.8M since the last report. We unfortunately experienced some principal loss on the grouping of repaid loans this period. While this is disappointing, we also have some REO properties that we think may be sold for more than our principal balance to help offset some of this loss. We remain committed to maximizing the total return of principal on this portfolio while also working towards providing liquidity as quickly as possible.

We started the period with 5 performing and 46 non-performing loans, 21 of which are now REO. We had one performing loan become non-performing. Two performing and 7 non-performing/REO loans repaid this period.

Please note that some loans are “portfolio” loans, meaning that they have more than one underlying property securing the loan. As the individual properties are sold/repaid, the portfolio loan remains “open” while liquidity is generated on the “partial release” of the underlying properties. This may skew the unit count numbers until all of the underlying properties of the portfolio loan are repaid and the loan is “closed”. The below tables show the movement of loan counts for the period.

Managing this portfolio and expediting loan repayments remains a high priority. We will continue to push forward on bringing this portfolio to a resolution.

Please consider the components of this analysis are incredibly dynamic as payoffs, loan sales, servicing advances and various reconciliation efforts are ongoing daily.

Borrower Dependent Notes (BDNs)

Since the last report, 11 BDN loans have been repaid, representing $4.4M of principal. To the extent that an underlying loan is making interest payments, we continue to process interest distributions 2-3 business days after they are received. If you have not received an interest payment on one of your BDN investments, this is because the underlying loan has not made its interest payment. Our team continues to reach out to past due borrowers and work them through our asset management and loss mitigation process.

We continue to strive to provide detailed and timely updates on all individual BDN investments while balancing the time spent on updates relative to focusing that time towards creating positive outcomes. In the last month we’ve posted updates on 61% of outstanding loans. We’ll continue to strive to provide additional updates on these investments and keep the information updated best we can. Please know that even if an update hasn’t been posted, we’re monitoring and working each loan towards a resolution.

RBNF

There was a moderate amount of liquidity created on underlying RBNF loans this period. A RBNF distribution will be processed this week. The balance of RBNF notes is $1.25M. The remaining balance is largely REO or late stage foreclosure. We continue to work on resolving the underlying loans to create liquidity for distributions on these notes.

Horizon

We continue to generate liquidity on the Horizon portfolio and expect to process another monthly distribution around the first week of April. We remain committed to managing the Horizon portfolio and maximizing the outcome for Horizon investors.

We appreciate your patience as we work to return capital to investors. We remain committed and optimistic that liquidity will continue to be created on the remaining portfolio. We ask that you continue to trust that we’re doing all that we can to get these resolved as quickly as practicable while trying to optimize the total return of capital.

Matt and The Upright Team

~~~~~~~~~~~~~~~~~~~~~~~~~~~~

March 6th, 2026

Dear Investors,

We received additional PFNF and RBNF proceeds shortly after our recent February distribution. As such, we are processing supplemental distributions of $1.5M for PFNF and ~$120K for RBNF. This represents 13.04% of the remaining PFNF note balance and brings the total percent returned to 85.76% since we began this distribution plan. We will post updated portfolio statistics and reconciliation per our usual schedule.

Thank you for your continued patience and understanding.

Matt and the Upright Team

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

February 24th, 2026

Dear Investors,

Below is an update as to where things stand with overall return of capital in the various Upright investment products. We appreciate your continued patience and will continue to provide updates here once per month.

PFNF

This week we will be initiating a PFNF principal distribution for $900K, which represents ~7.26% of the remaining PFNF note balance. We’ve now returned 83.63% of all PFNF principal since we began this distribution plan.

The portfolio continues to make progress through the foreclosure to REO and final disposition process. In the last month, five properties had winning bids at auction by 3rd party buyers. This is a good outcome both in terms of total recovery as well as time to disposition. We are also continuing to run parallel disposition strategies (i.e. loan sales, bulk REO sales, workouts, etc.) on the portfolio where and when it makes sense. We remain optimistic that liquidity will continue to be created on the underlying assets in the coming months.

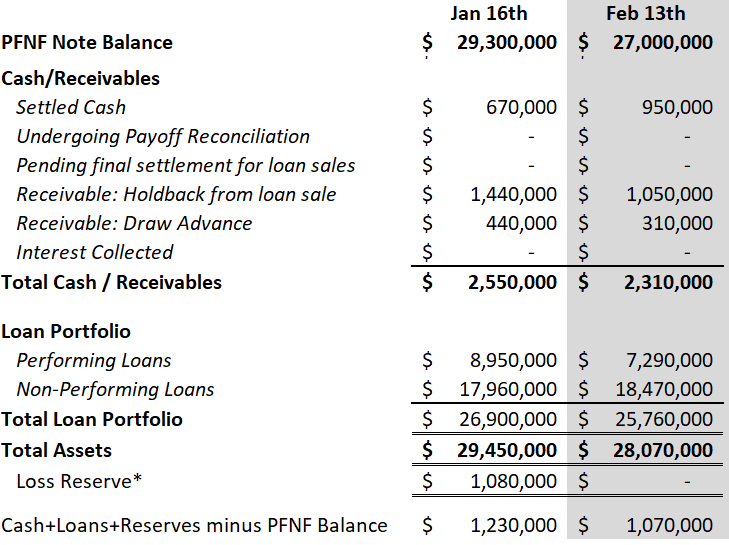

The below is a current snapshot of where remaining PFNF funds are allocated relative to last time this was reported. Please note that the below figures are inclusive of the $350k distribution that was processed on February 5th.

The overall loan portfolio decreased by ~$1.2M since the last report. We unfortunately experienced some principal loss on the grouping of repaid loans this period. While this is disappointing, we also have some REO properties that we think will be sold for more than our principal balance to help offset some of this loss. We remain committed to maximizing the total return of principal on this portfolio while also working towards providing liquidity as quickly as possible.

We started the period with 6 performing and 47 non-performing loans, 22 of which are now REO. We had no performing loans become non-performing. One performing and 1 non-performing/REO loans repaid this period.

Please note that some loans are “portfolio” loans, meaning that they have more than one underlying property securing the loan. As the individual properties are sold/repaid, the portfolio loan remains “open” while liquidity is generated on the “partial release” of the underlying properties. This may skew the unit count numbers until all of the underlying properties of the portfolio loan are repaid and the loan is “closed”. (i.e. For this period, we had more than 2 properties/loans repay, as some of the liquidity is associated with portfolio loans.) The below tables show the movement of loan counts for the period.

Managing this portfolio and expediting loan repayments remains a high priority. We will continue to push forward on bringing this portfolio to a resolution.

Please consider the components of this analysis are incredibly dynamic as payoffs, loan sales, servicing advances and various reconciliation efforts are ongoing daily.

Borrower Dependent Notes (BDNs)

Since the last report, 9 BDN loans have been repaid, representing $2.2M of principal. To the extent that an underlying loan is making interest payments, we continue to process interest distributions 2-3 business days after they are received. If you have not received an interest payment on one of your BDN investments, this is because the underlying loan has not made its interest payment. Our team continues to reach out to past due borrowers and work them through our asset management and loss mitigation process.

We continue to strive to provide detailed and timely updates on all individual BDN investments while balancing the time spent on updates relative to focusing that time towards creating positive outcomes. In the last month we’ve posted updates on 53% of outstanding loans. We’ll continue to strive to provide additional updates on these investments and keep the information updated best we can. Please know that even if an update hasn’t been posted, we’re monitoring and working each loan towards a resolution.

RBNF

There was a moderate amount of liquidity created on underlying RBNF loans this period. A RBNF distribution will be processed this week. The balance of RBNF notes is $1.43M. The remaining balance is largely REO or late stage foreclosure. We continue to work on resolving the underlying loans to create liquidity for distributions on these notes.

Horizon

The 2026 Q4 financials will be shared with Horizon investors in the coming week. We also expect to process another monthly distribution around the first week of March. We continue to be committed to managing the Horizon portfolio and maximizing the outcome for Horizon investors.

We appreciate your patience as we work to return capital to investors. We remain committed and optimistic that liquidity will continue to be created on the remaining portfolio. We ask that you continue to trust that we’re doing all that we can to get these resolved as quickly as practicable while trying to optimize the total return of capital.

Matt and The Upright Team

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

February 5th, 2026

Dear Investors,

The month of January was a particularly slow month for loan repayments. The year-end holidays combined with an end-of-the-month snow storm impacted a good number of in-person closings. We expect activity to pick back up in February, and are expecting some loan/REO dispositions in the coming weeks.

Given there hasn’t been much movement in the overall loan count or balances, we are deferring the full monthly update until we have more month-over-month change to report. That said, we do have a moderate amount of PFNF liquidity that was created via single property dispositions in portfolio loans. As such, we will be processing a $350k PFNF distribution this week, which represents ~2.75% of the remaining balance. We will post a more complete update with the next PFNF distribution which we believe will be more substantive as additional payoffs are expected in the coming weeks.

Thanks for your continued patience.

Matt and the Upright Team

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

January 7th, 2026

Dear Investors,

Below is an update as to where things stand with overall return of capital in the various Upright investment products. We appreciate your continued patience and will continue to provide updates here once per month.

PFNF

This week we will be initiating a PFNF principal distribution for $900K, which represents ~6.6% of the remaining PFNF note balance. We’ve now returned 81.85% of all PFNF principal since we began this distribution plan. We have several REO properties scheduled to close in the late part of this month that we expect to generate another ~1.0-$1.5M of liquidity. As we’ve done in previous months, if additional liquidity is generated in the next couple of weeks, we will process a supplemental distribution this month.

We remain optimistic that liquidity will continue to be created on the underlying assets in the coming months. The portfolio continues to make progress through the foreclosure to REO and final disposition process. We are also continuing to run parallel disposition strategies (i.e. loan sales, bulk REO sales, workouts, etc.) on the portfolio where and when it makes sense.

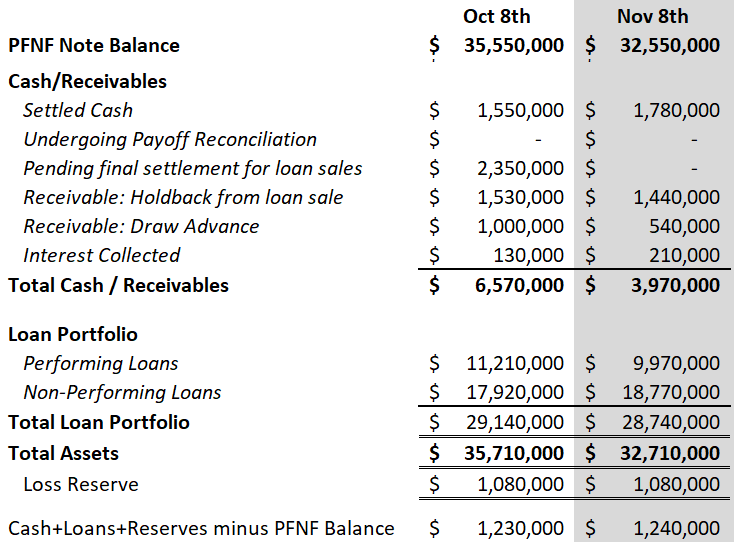

The below is a current snapshot of where remaining PFNF funds are allocated relative to last time this was reported. Please note that REOs are being reported separately from NPLs again this month.

The overall loan portfolio decreased by ~$3.8M since the last report. We unfortunately experienced some principal loss on the grouping of repaid loans this period. While this is disappointing, we also have some REO properties that we think will be sold for more than our principal balance to help offset some of this loss. We remain committed to maximizing the total return of principal on this portfolio while also working towards providing liquidity as quickly as possible.

We started the period with 6 performing and 52 non-performing loans, 23 of which are now REO. We had no performing loans become non-performing. No performing and 5 non-performing/REO loans repaid this period.

Please note that some loans are “portfolio” loans, meaning that they have more than one underlying property securing the loan. As the individual properties are sold/repaid, the portfolio loan remains “open” while liquidity is generated on the “partial release” of the underlying properties. This may skew the unit count numbers until all of the underlying properties of the portfolio loan are repaid and the loan is “closed”. (i.e. For this period, we likely had more than 5 properties/loans repay, as some of the liquidity is associated with portfolio loans.) The below tables show the movement of loan counts for the period.

Managing this portfolio and expediting loan repayments remains a high priority. We will continue to push forward on bringing this portfolio to a resolution.

Please consider the components of this analysis are incredibly dynamic as payoffs, loan sales, servicing advances and various reconciliation efforts are ongoing daily.

Borrower Dependent Notes (BDNs)

In the last month, 9 BDN loans have been repaid, representing $9.5M of principal. To the extent that an underlying loan is making interest payments, we continue to process interest distributions 2-3 business days after they are received. If you have not received an interest payment on one of your BDN investments, this is because the underlying loan has not made its interest payment. Our team continues to reach out to past due borrowers and work them through our asset management and loss mitigation process.

We continue to strive to provide detailed and timely updates on all individual BDN investments while balancing the time spent on updates relative to focusing that time towards creating positive outcomes. In the last month we’ve posted updates on 68% of outstanding loans. We’ll continue to strive to provide additional updates on these investments and keep the information updated best we can. Please know that even if an update hasn’t been posted, we’re monitoring and working each loan towards a resolution.

RBNF

There were no RBNF loans repaid during this period. The balance of RBNF notes is $1.45M. The remaining balance is largely REO or late stage foreclosure. We continue to work on resolving the underlying loans to create liquidity for distributions on these notes.

Horizon

We are working on preparing Q4 financials and will share with Horizon investors next month. We also recently processed another monthly distribution and an updated monthly report. We continue to be committed to managing the Horizon portfolio and maximizing the outcome for Horizon investors.

We appreciate your patience as we work to return capital to investors. We remain optimistic that the recent momentum will continue in Q1 of the new year. We ask that you continue to trust that we’re doing all that we can to get these resolved as quickly as practicable while trying to optimize the total return of capital.

Matt and The Upright Team

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

December 11th, 2025

Dear Investors,

As communicated in the last update, we have received additional funds on the PFNF portfolio and have now completed the reconciliation. As such, we are processing a $2M supplemental distribution today. This represents 12.78% of the remaining PFNF note balance and brings the total percent returned to 80.57% since we began this distribution plan. We will post updated portfolio statistics and reconciliation per our usual schedule.

Thank you for your continued patience and understanding.

Matt and the Upright Team

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

December 5th, 2025

Dear Investors,

We appreciate your patience as we’re a bit behind schedule this month with the Thanksgiving holiday. Below is an update as to where things stand with overall return of capital in the various Upright investment products.

PFNF

This week we will be initiating a PFNF principal distribution for $400K, which represents ~2.5% of the remaining PFNF note balance. We’ve now returned 77.72% of all PFNF principal since we began this distribution plan. We expect to process a follow-up distribution next week for ~$2M which will bring the total percent returned to ~80.6%. We received funds in escrow earlier this week for several more loan/REO dispositions that we are waiting to be released subject to clearing all final conditions. Given we are already a week behind schedule on the update, we wanted to get something out this week. Interest collected on the portfolio this period was $10,090 and has been included in the distribution.

We continue to be optimistic that the uptick in recent liquidity will continue through the end of the year and into the early part of next year. In addition to the recent payoffs, we have also continued to make progress on working additional loans towards dispositions, particularly with properties that are now REO. We currently have ~$5M of PFNF loans that are REO and listed or under contract to be sold. Our current forecast expects to have another ~$1M+/- resolve before the end of the year. We also continue to advance more loans through the foreclosure process and have gotten them to REO status which brings us closer to final disposition as well. We are also continuing to run parallel disposition strategies (i.e. loan sales, bulk REO sales, workouts, etc.) on the portfolio where and when it makes sense.

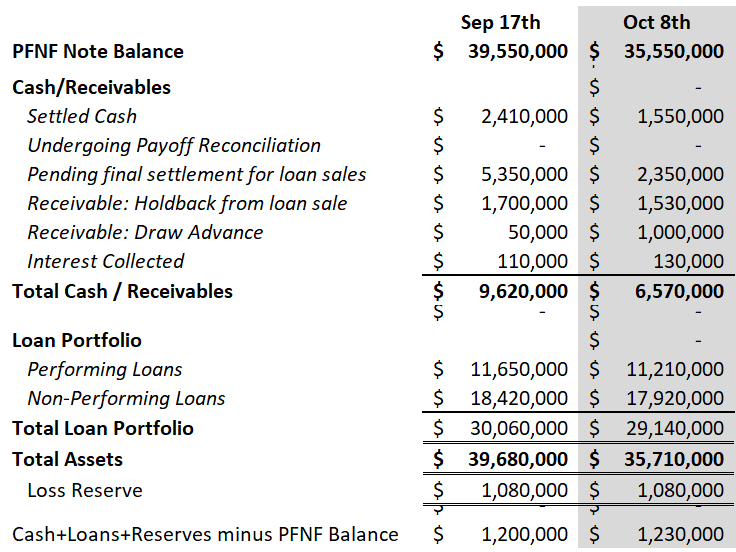

The below is a current snapshot of where remaining PFNF funds are allocated relative to last time this was reported. Please note that REOs are being reported separately from NPLs again this month.

The overall loan portfolio decreased by ~$400K in the last month. We started the period with 6 performing and 58 non-performing loans, 18 of which are now REO. We had no performing loans become non-performing. No performing and 6 non-performing/REO loans repaid this period.

Please note that some loans are “portfolio” loans, meaning that they have more than one underlying property securing the loan. As the individual properties are sold/repaid, the portfolio loan remains “open” while liquidity is generated on the “partial release” of the underlying properties. This may skew the unit count numbers until all of the underlying properties of the portfolio loan are repaid and the loan is “closed”. The below tables show the movement of loan counts for the period.

Managing this portfolio and expediting loan repayments remains a high priority. We will continue to push forward on bringing this portfolio to a resolution.

Please consider the components of this analysis are incredibly dynamic as payoffs, loan sales, servicing advances and various reconciliation efforts are ongoing daily.

Borrower Dependent Notes (BDNs)

In the last month, 6 BDN loans have been repaid, representing $3.1M of principal. To the extent that an underlying loan is making interest payments, we continue to process interest distributions 2-3 business days after they are received. If you have not received an interest payment on one of your BDN investments, this is because the underlying loan has not made its interest payment. Our team continues to reach out to past due borrowers and work them through our asset management and loss mitigation process.

We continue to strive to provide detailed and timely updates on all individual BDN investments while balancing the time spent on updates relative to focusing that time towards creating positive outcomes. In the last month we’ve posted updates on 59% of outstanding loans. We’ll continue to strive to provide additional updates on these investments and keep the information updated best we can. Please know that even if an update hasn’t been posted, we’re monitoring and working each loan towards a resolution.

RBNF

There were no RBNF loans repaid during this period. The balance of RBNF notes is $1.64M. We now have ~$250k of this balance under contract to be sold. The remaining balance is largely REO or late stage foreclosure. We continue to work on resolving the underlying loans to create liquidity for distributions on these notes.

Horizon

Q3 financials were shared last month and sent to all Horizon investors. We also recently processed another monthly distribution and an updated monthly report. We continue to be committed to managing the Horizon portfolio and maximizing the outcome for Horizon investors.

We appreciate your patience as we work to return capital to investors. We remain optimistic that the momentum of Q4 will continue. We ask that you continue to trust that we’re doing all that we can to get these resolved as quickly as practicable while trying to optimize the total return of capital.

Matt and The Upright Team

~~~~~~~~~~~~~~~~~~~~~~~

October 31st, 2025

PFNF

Today we will be initiating a PFNF principal distribution for $2M, which represents ~11.08% of the remaining PFNF note balance. Inclusive of the $2.4M off-cycle distribution made at the beginning of the month, we’ve now returned 77.15% of all PFNF principal since we began this distribution plan. Interest collected on the portfolio this period was $13,520 and has been included in the distribution.

We’re optimistic that the uptick in recent liquidity will continue through the end of the year and we remain focused on working these loans/REOs through to final disposition. In addition to the recent payoffs, we have also continued to make progress on working additional loans towards dispositions, particularly with properties that are now REO. We currently have ~$5M of PFNF loans that are REO and listed or under contract to be sold. We expect some of these to close in November. We also continue to advance more loans through the foreclosure process and have gotten them to REO status which brings us closer to final disposition as well. We are also continuing to run parallel disposition strategies (i.e. loan sales, bulk REO sales, workouts, etc.) on the portfolio where and when it makes sense

The below is a current snapshot of where remaining PFNF funds are allocated relative to last time this was reported. Please note that REOs are being reported separately from NPLs again this month.

The overall loan portfolio decreased by $4.5M in the last month. We started the period with 8 performing and 63 non-performing loans, 24 of which are now REO. We had one performing loan become non-performing. One performing and 6 non-performing/REO loans repaid this period. The below tables show the movement of loan counts for the period.

Please note that some loans are “portfolio” loans, meaning that they have more than one underlying property securing the loan. As the individual properties are sold/repaid, the portfolio loan remains “open” while liquidity is generated on the “partial release” of the underlying properties. This may skew the unit count numbers until all of the underlying properties of the portfolio loan are repaid and the loan is “closed”.

Managing this portfolio and expediting loan repayments remains a high priority. We will continue to push forward on bringing this portfolio to a resolution.

Please consider the components of this analysis are incredibly dynamic as payoffs, loan sales, servicing advances and various reconciliation efforts are ongoing daily.

Borrower Dependent Notes (BDNs)

In the last month, 6 BDN loans have been repaid, representing $3.1M of principal. To the extent that an underlying loan is making interest payments, we continue to process interest distributions 2-3 business days after they are received. If you have not received an interest payment on one of your BDN investments, this is because the underlying loan has not made its interest payment. Our team continues to reach out to past due borrowers and work them through our asset management and loss mitigation process.

We continue to strive to provide detailed and timely updates on all individual BDN investments while balancing the time spent on updates relative to focusing that time towards creating positive outcomes. In the last month we’ve posted updates on 53% of outstanding loans. We’ll continue to strive to provide additional updates on these investments and keep the information updated best we can. Please know that even if an update hasn’t been posted, we’re monitoring and working each loan towards a resolution.

RBNF

There were four RBNF loans repaid during this period, providing a return of capital of ~$275.4k which will be distributed to investors pro rata in the coming days. The balance of RBNF notes is now $1.45M. The remaining balance is largely REO or late stage foreclosure, meaning we expect an increase in dispositions through the end of the year. We continue to work on resolving the underlying loans to create liquidity for distributions on these notes.

Horizon

We expect to complete Q3 financials in the coming weeks along with the next distribution. An updated monthly report will be provided to all Horizon investors concurrently with the next distribution. We continue to be committed to managing the Horizon portfolio and maximizing the outcome for Horizon investors.

We appreciate your patience as we work to return capital to investors. We remain optimistic that the momentum of October will carry on through the end of the year. We ask that you continue to trust that we’re doing all that we can to get these resolved as quickly as practicable while trying to optimize the total return of capital.

Matt and The Upright Team

~~~~~~~~~~~~~~~~~~

October 7th, 2025

Dear Investors,

As we hoped we would, we had a reasonable amount of payoffs/REO sales on the underlying PFNF portfolio at the end of September and first week of October. As a result, we are processing a supplemental PFNF distribution of $2.4M this week. This represents 11.73% of the remaining PFNF note balance and brings the total percent returned to 74.30% since we began this distribution plan. We will post updated portfolio statistics and reconciliation at the end of October per our usual schedule.

Thank you for your continued patience and understanding.

Matt and the Upright Team

~~~~~~~~~~~~~~~~~~~~~~~~~

September 26th, 2025

Dear Investors,

Below is an update as to where things stand with overall return of capital in the various Upright investment products. We appreciate your continued patience and will continue to provide updates here once per month.

PFNF

This week we will be initiating a PFNF principal distribution for $400k, which represents ~1.92% of the remaining PFNF note balance. We’ve now returned 70.9% of all PFNF principal since we began this distribution plan. Interest collected on the portfolio this period was $17,859 and has been included in the distribution.

We realize this makes for another month of disappointing results on generating liquidity on the underlying portfolio. While we were hopeful that we’d have more REO dispositions and other payoffs come in before the end of the month, a good number of closings have been pushed into next month for a variety of reasons. We continue to work with buyers, borrowers and related service providers to work these to a final disposition.

If we receive additional proceeds from loan/REO dispositions in the coming weeks, we will process a follow-on distribution as quickly as we can. We’re optimistic that we’ll have more to distribute in the next couple of weeks.

We have continued to make progress on working additional loans towards dispositions, particularly with properties that are now REO. We now have 16 PFNF loans (~$4.5M) that are REO and under contract to be sold. We’ve also advanced several more loans through the foreclosure process and gotten them to REO status which brings us closer to final disposition as well. (For more information on the REO process, please refer to July’s update.)

We also continue to work with the loan buyer on the portfolio sale mentioned in prior updates, as well as a few other loan buyers we’ve since engaged. Given that many of these loans are in later-stage default and/or are now REOs, the depth of diligence and amount of moving parts has resulted in a slower process than initially anticipated. We intend to continue to move forward and will likely transact on a loan-by-loan basis as diligence clears and where it still makes sense. We are also working parallel disposition strategies on all of these loans to ensure these continue to move towards a resolution.

We share your disappointment that we don’t have more to distribute this month, and appreciate that this “we’re close” messaging is getting tiring. We want nothing more than to be able to write a more positive update and continue to work tirelessly to produce liquidity on this underlying portfolio. We’re very grateful for your patience and understanding and once again ask for this to continue so we can remain focused on getting the results we all want.

The below is a current snapshot of where remaining PFNF funds are allocated relative to last time this was reported. Please note that REOs are being reported separately from NPLs again this month.

The overall loan portfolio decreased by $290k in the last month. We started the period with 10 performing and 67 non-performing loans, 23 of which are now REO. We had no loans go from NPL to performing and one performing loan became non-performing. One performing and 5 non-performing loans repaid this period. The below tables show the movement of loan counts for the period.

Managing this portfolio and expediting loan repayments remains a high priority. We will continue to push forward on the loan sale and other strategies to create liquidity where possible.

Please consider the components of this analysis are incredibly dynamic as payoffs, loan sales, servicing advances and various reconciliation efforts are ongoing daily.

Borrower Dependent Notes (BDNs)

In the last month, 9 BDN loans have been repaid, representing $2.7M of principal. To the extent that an underlying loan is making interest payments, we continue to process interest distributions 2-3 business days after they are received. If you have not received an interest payment on one of your BDN investments, this is because the underlying loan has not made its interest payment. Our team continues to reach out to past due borrowers and work them through our asset management and loss mitigation process.

We continue to strive to provide detailed and timely updates on all individual BDN investments while balancing the time spent on updates relative to focusing that time towards creating positive outcomes. In the last month we’ve posted updates on 66% of outstanding loans. We’re continuing to focus on those that are behind on either payments or maturity date. We’ll continue to strive to provide additional updates on these investments and keep the information updated best we can. Please know that even if an update hasn’t been posted, we’re monitoring and working each loan towards a resolution.

RBNF

There was one RBNF loan repaid during this period, providing a return of capital of ~$17.5k which will be distributed to investors pro rata in the coming days. The balance of RBNF notes is now $1.727M. We now have ~$500k of this balance under contract to be sold. The remaining balance is largely REO or late stage foreclosure, meaning we expect an increase in dispositions through the end of the year. We continue to work on resolving the underlying loans to create liquidity for distributions on these notes.

Horizon

We’ve begun preparing Q3 financials and the next distribution, which we expect to process in the coming weeks. An updated monthly report will be provided to all Horizon investors concurrently with the next distribution. We continue to be committed to managing the Horizon portfolio and maximizing the outcome for Horizon investors.

We appreciate your patience as we work to return capital to investors. I’m optimistic that we’ll have some additional capital to return throughout October as we have committed closings on the books for a good number of loans/REOs. We ask that you continue to trust that we’re doing all that we can to get these resolved as quickly as practicable while trying to optimize the total return of capital.

Matt and The Upright Team

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

August 28th, 2025

PFNF

Over the past month we’ve had just 3 underlying loans repay that are part of the PFNF portfolio, representing ~$167k in principal. Concurrently, we also advanced ~$190k in the underlying portfolio as protective servicing advances (taxes, insurance, property preservation, renovations, etc. As a reminder, these servicing advances are “first out” when the underlying loan is repaid.)

As a result, and for the first time since we started this plan, we unfortunately do not have any liquidity to process a distribution this month.

While it is disappointing that we don’t have more liquidity this month, we have continued to make progress on working towards loan dispositions, particularly with properties that are now REO. We now have 13 PFNF loans (~$4M) that are REO and under contract to be sold, with expected closing dates in the next ~30 days. We’ve also advanced several more loans through the foreclosure process and gotten them to REO status which brings us closer to final disposition as well. (For more information on the REO process, please refer to last month’s update.)

We also continue to work with the loan buyer on the portfolio sale mentioned last month. As diligence progresses and certain loans move through legal proceedings, the number of loans available for sale as well as their pricing is somewhat dynamic. For example, it is challenging to sell a loan where the foreclosure auction is imminent. We do not want to delay any foreclosure auctions so we are adjusting our loan sale plan accordingly. As a result, we’ll likely be breaking the loan sale into smaller increments and dispositioning the ones we can over the coming months. We’re still working on getting the first transaction done sometime in September.

We share your disappointment that we don’t have more to distribute this month, and we hope that you appreciate we are making meaningful progress, even if it's not yet showing up in distributable proceeds. We continue to expect the pace of the distributions to pick-up in the coming months as we work to get these loans across the finish-line.

For what its worth, payoffs were down by ~50% across our entire portfolio this month. Speaking with some of our institutional loan buyers and other market participants, most of them also experienced a slow down in payoffs across their portfolios in August. We’re hopeful that as folks return from their summer vacations (borrowers, buyers, agents, title companies, etc.) the pace of transactions will revert to the mean.

The below is a current snapshot of where remaining PFNF funds are allocated relative to last time this was reported. Please note that REOs are being reported separately from NPLs again this month.

The overall loan portfolio increased $20k in the last month as a result of protective advances being greater than the amount of payoffs received, as outlined above. We started the period with 11 performing and 69 non-performing loans, 25 of which are now REO. We had no loans go from NPL to performing and one performing loan became non-performing. No performing and 3 non-performing loans repaid this period. The below tables show the movement of loan counts for the period.

Managing this portfolio and expediting loan repayments remains a high priority. We will continue to push forward on the loan sale and other strategies to create liquidity where possible.

Please consider the components of this analysis are incredibly dynamic as payoffs, loan sales, servicing advances and various reconciliation efforts are ongoing daily.

Borrower Dependent Notes (BDNs)

In the last month, 5 BDN loans have been repaid, representing $500K of principal. To the extent that an underlying loan is making interest payments, we continue to process interest distributions 2-3 business days after they are received. If you have not received an interest payment on one of your BDN investments, this is because the underlying loan has not made its interest payment. Our team continues to reach out to past due borrowers and work them through our asset management and loss mitigation process.

We continue to strive to provide detailed and timely updates on all individual BDN investments while balancing the time spent on updates relative to focusing that time towards creating positive outcomes. In the last month we’ve posted updates on 59% of outstanding loans. We’re continuing to focus on those that are behind on either payments or maturity date. We’ll continue to strive to provide additional updates on these investments and keep the information updated best we can. Please know that even if an update hasn’t been posted, we’re monitoring and working each loan towards a resolution.

RBNF

As mentioned last month, we are working through a loan sale. The RBNF portfolio has 6 loans representing $554k of principal balance that we are working on closing in increments over the coming months. Otherwise, there haven’t been any payoffs for loans in which RBNF holds a position in the last month. The balance on RBNF notes is $1.744M. The remaining underlying loans that support this balance are all in later-stage default and being worked on by the asset management team. We continue to work on resolving the underlying loans to create liquidity for distributions on these notes.

Horizon

Second quarter financials and reporting were posted in the last month and can be reviewed here. We continue to be committed to managing the Horizon portfolio and maximizing the outcome for Horizon investors.

We appreciate your patience and understanding as we work to return capital to investors. I can appreciate the continued frustration as it relates to how long it is taking to resolve some of the loans. I ask that you continue to trust that we’re doing all that we can to get these resolved as quickly as practicable while trying to optimize the total return of capital. I’m optimistic that future updates will have better results to share related to liquidity creation on the underlying portfolios.

Matt and The Upright Team

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

July 25th, 2025

PFNF

This week we will be initiating a PFNF principal distribution for $500k, which represents ~2.3% of the remaining PFNF note balance. We’ve now returned 70.32% of all PFNF principal since we began this distribution plan. Interest collected on the portfolio this period was $11,666 and has been included in the distribution.

We realize this makes several months in-a-row of disappointing results on generating liquidity on the underlying portfolio. Unfortunately, what largely remains are loans that are now going through the foreclosure and REO process. When a loan reaches this stage, it takes longer to resolve as a matter of legal policy and procedure that must be followed. That said, as further outlined below, we are taking active measures to speed up the pace of liquidity where we can.

As one measure to expedite liquidity on these loans, we’ve been exploring a bulk sale of certain non-performing loans and REOs. As of this week, we have entered into a Letter of Intent (LOI) to sell a portfolio of loans, of which ~$4M of PFNF capital across 24 loans will be sold. We are working earnestly with the loan buyer to complete loan-level due diligence and definitive agreements to consummate the sale as quickly as we can. Realistically, the sale will likely take place sometime in late August or September. Based on indicative pricing, we’re expecting a manageable principal write down on this portfolio relative to our reserve. Final pricing will be provided as final diligence is complete in the coming weeks.

While the liquidity we would have liked wasn’t created this month, we are making progress on getting loans through the foreclosure process. As shown below, $9.88M (56%) of the non-performing portfolio is now Real Estate Owned (REO). This means we now hold title to the properties and are able to begin moving them through the readiness, listing, and sale process.

In the table below we’ve provided additional data points related to the principal balance and count of loans that are now REO. While this is a meaningful milestone which brings us much closer to disposition and liquidity, there remain some procedural steps that need to be followed:

-

Ratification of Sale: This varies by jurisdiction, but after the foreclosure sale, there is anywhere from a week to a month or more for the local jurisdiction to ratify the sale at auction. During this time, the jurisdiction typically produces a bill of sale which ensures that any “super liens”—such as water, sewer, taxes, foreclosure costs, etc.—are paid.

-

Record Deed: Once the bill of sale has been paid and the sale ratified, the local governing authority (often the sheriff's office) must record the foreclosure deed, registering the new owner in the public record. Again, depending on the jurisdiction, this can be as quick as one week or take several months. (An extreme example of this right now is the City of Philadelphia, which has a backlog of several months, in part caused by a worker shortage and antiquated systems at the sheriff’s office.) Once the deed is recorded, as the winning credit bidder of the foreclosure auction, we become the official owner of the property.

-

Prepare Property for Sale: Depending on the condition of the property, we must then prepare the property for sale, ensuring it is safe, secure and uninhabited. To the extent it makes sense for maximizing value, we may also choose to complete repairs or improvements prior to listing. This can sometimes happen in parallel with the previous two steps and other times we must wait to officially take possession prior to starting this step. Again, depending on the condition of the property this can be a couple of weeks to several months.

-

List and Negotiate Sale: Once the property is ready for sale, it is listed with a local broker and we begin accepting offers. As per any real estate sale, this often includes negotiating price, deposit, closing timelines, contingencies, etc. all in an effort to maximize recovery and certainty of closing. Depending on the property and market conditions, this can be weeks to months.

-

Close: After agreeable terms have been reached with a buyer and a purchase and sale agreement signed, there is typically 2-4 weeks granted for the buyer to close the transaction. This provides them time to line-up financing, title insurance, property/casualty insurance, etc. At the end of this agreed upon time, the property is transferred and we receive our proceeds which are subsequently distributed to investors.

All of the above is to demonstrate that while reaching REO is a big step towards final resolution, there remain steps and time to get to final disposition. We are managing each of these properties closely and pushing them forward as quickly as we can through each step. It should also be noted that some of the REOs are further along in the process than others and we expect some liquidity on these sooner than later. More specifically we have $3-4M that are not included on the NPL tape that are either listed or we expect to have listed in the coming weeks.

As a final point, in the last month, we completed construction on 8 properties in which PFNF had a total position of $1M+. We invested ~$250k of capital to bring these properties to sale-ready. We believe that in doing so, not only will we recover our principal and interest, but there is potential for an additional gain, which will accrue to PFNF holders pro-rata. These properties are currently being listed and we expect them to begin creating liquidity as they are sold in the coming months.

While we share in your disappointment that we don’t have more to distribute this month, we hope that you appreciate we are continuing to press forward and are making meaningful progress. We expect the pace of the distributions to pick-up in the coming months as we work to get these loans across the finish-line.

The below is a current snapshot of where remaining PFNF funds are allocated relative to last time this was reported. Please note that REOs are being reported separately from NPLs for the first time this month.

The overall loan portfolio has been reduced by $310k in the last month. We started the period with 13 performing and 71 non-performing loans, 21 of which are now REO. We had no loans go from NPL to performing and two performing loans became non-performing. No performing and four non-performing loans repaid this period. The below tables show the movement of loan counts for the period.

Managing this portfolio and expediting loan repayments remains a high priority. We will continue to push forward on the loan sale and other strategies to create liquidity where possible.

Please consider the components of this analysis are incredibly dynamic as payoffs, loan sales, servicing advances and various reconciliation efforts are ongoing daily.

Borrower Dependent Notes (BDNs)

In the last month, 5 BDN loans have been repaid, representing $1.26M of principal. To the extent that an underlying loan is making interest payments, we continue to process interest distributions 2-3 business days after they are received. If you have not received an interest payment on one of your BDN investments, this is because the underlying loan has not made its interest payment. Our team continues to reach out to past due borrowers and work them through our asset management and loss mitigation process.

We continue to strive to provide detailed and timely updates on all individual BDN investments while balancing the time spent on updates relative to focusing that time towards creating positive outcomes. In the last month we’ve posted updates on 67% of outstanding loans. We’re continuing to focus on those that are behind on either payments or maturity date. We’ll continue to strive to provide additional updates on these investments and keep the information updated best we can. Please know that even if an update hasn’t been posted, we’re monitoring and working each loan towards a resolution.

RBNF

As mentioned previously, we are working through a loan sale. The RBNF portfolio has 6 loans representing $554k of principal balance that we are working on closing in late August or September. Otherwise, there haven’t been any payoffs for loans in which RBNF holds a position in the last month. The balance on RBNF notes is $1.744M. The remaining underlying loans that support this balance are all in later-stage default and being worked on by the asset management team. We continue to work on resolving the underlying loans to create liquidity for distributions on these notes.

Horizon

We are currently working on completing the Q2 financials and reporting package for Horizon. We expect to have this done in Mid-August per our usual schedule, after which the Q2 distribution will be processed.

We continue to appreciate your patience and understanding as we work to return capital to investors. I can appreciate the frustration as it relates to how long it is taking to resolve some of the loans. I ask for your continued trust that we’re doing all that we can to get these resolved as quickly as practicable while trying to optimize the total return of capital.

Matt and The Upright Team

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

June 24th, 2025

Dear Investors,

Below is an update as to where things stand with overall return of capital in the various Upright investment products. We appreciate your continued patience and will continue to provide updates here once per month.

PFNF

This week we will be initiating a PFNF principal distribution for $500k, which represents ~2.3% of the remaining PFNF note balance. We’ve now returned 69.6% of all PFNF principal since we began this distribution plan. Interest collected on the portfolio this period was $22,509 and has been included in the distribution.

We unfortunately had another slower month than we hoped as it relates to payoffs and NPL resolutions on the PFNF portfolio. We continue to believe that we’re getting close to resolutions on a number of the loans that we’ve been working towards final payoff. We’ll continue to press forward on this front and are optimistic in our outlook for more payoff activity in the coming months.

While not a source for immediate liquidity, similar to last month, we have recently completed the foreclosure process on 6 properties representing $1M of principal. Depending on the jurisdiction, it will take several weeks to record the foreclosure deed, after which we’ll be proceeding with the process to sell them. While this doesn’t create immediate liquidity for distribution, it is a meaningful milestone towards providing a final resolution on these loans. As these loans get listed and sold, we expect more liquidity to become available in the coming months.

Additionally, we are in the process of marketing for sale certain non-performing loan inventory. To date, we have received one bid that we think could be viable which we are further analyzing and negotiating. Should this come to fruition, it will provide a much more certain and timely path to resolution on a number of loans.

The below is a current snapshot of where remaining PFNF funds are allocated relative to last time this was reported.

The overall loan portfolio has been reduced by $300k in the last month. We started the period with 16 performing and 70 non-performing loans. We had no loans go from NPL to performing and two performing loans became non-performing. One performing and one non-performing loan repaid this period. The below tables show the movement of loan counts for the period.

Managing this portfolio and expediting loan repayments remains a high priority. Nearly half of our 20 person team is involved on a daily basis in some form of working these loans towards a resolution.

Please consider the components of this analysis are incredibly dynamic as payoffs, loan sales, servicing advances and various reconciliation efforts are ongoing daily.

Borrower Dependent Notes (BDNs)

In the last month, 5 BDN loans have been repaid, representing $1.6M of principal. To the extent that an underlying loan is making interest payments, we continue to process interest distributions 2-3 business days after they are received. If you have not received an interest payment on one of your BDN investments, this is because the underlying loan has not made its interest payment. Our team continues to reach out to past due borrowers and work them through our asset management and loss mitigation process.

We continue to strive to provide detailed and timely updates on all individual BDN investments while balancing the time spent on updates relative to focusing that time towards creating positive outcomes. In the last month we’ve posted updates on 62% of outstanding loans. We’re continuing to focus on those that are behind on either payments or maturity date. We’ll continue to strive to provide additional updates on these investments and keep the information updated best we can. Please know that even if an update hasn’t been posted, we’re monitoring and working each loan towards a resolution.

RBNF

There haven’t been any payoffs for loans in which RBNF holds a position in the last month. The balance on RBNF notes is $1.744M. The remaining underlying loans that support this balance are all in later-stage default and being worked on by the asset management team. We continue to work on resolving the underlying loans to create liquidity for distributions on these notes.

Horizon

The Q1 2025 report was recently posted, which you can review here. We continue to see quarter over quarter improvement to returns.

The Fund is currently open and accepting new investments, with the next admittance date scheduled for July 1st, 2025. We’ve been purchasing new loans into the Fund as we are returning to market on the origination side of our business.

We continue to appreciate your support, understanding and patience as we work to return capital to investors. We look forward to continuing to serve.

Matt and The Upright Team

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

May 28th, 2025

Dear Investors,

Below is an update as we continue to make progress on our plans to return capital to investors while simultaneously rebuilding our origination capabilities for the long-term success of the Company. We appreciate your continued support and will continue to provide updates here once per month.

PFNF

This week we will be initiating a PFNF principal distribution for $1.0M, which represents ~4.38% of the remaining PFNF note balance. We’ve now returned 68.9% of all PFNF principal since we began this distribution plan. Interest collected on the portfolio this period was $17,670 and has been included in the distribution.

We unfortunately had a slower month than we hoped as it relates to payoffs and NPL resolutions on the PFNF portfolio. We do believe that we’re getting close to resolutions on a number of the loans that we’ve been working towards final payoff. Of particular note, we have recently completed the foreclosure process on 14 properties representing $4.4M of principal. Depending on the jurisdiction, it will take several weeks to record the deed, after which we’ll be proceeding with the process to sell them. This is a meaningful milestone towards creating additional liquidity on the non-performing portfolio. We’ll continue to press forward on this front and are optimistic in our outlook for more payoff activity in the coming months.

The below is a current snapshot of where remaining PFNF funds are allocated relative to last time this was reported.

The overall loan portfolio has been reduced by $790k in the last month. We started the period with 20 performing and 68 non-performing loans. We had no loans go from NPL to performing and three performing loans became non-performing. One performing and one non-performing loan repaid this period. We also had several loans partially repay, which explains why there is a $790k reduction while only having a total of 2 repaid loans. This happens when there is more than one property in a loan and they sell at different times. The below tables show the movement of loan counts for the period.

Managing this portfolio and expediting loan repayments remains a high priority. Nearly half of our 20 person team is involved on a daily basis in some form of working these loans towards a resolution.

Please consider the components of this analysis are incredibly dynamic as payoffs, loan sales, servicing advances and various reconciliation efforts are ongoing daily.

Borrower Dependent Notes (BDNs)

In the last month, 7 BDN loans have been repaid, representing $1.2M of principal. To the extent that an underlying loan is making interest payments, we continue to process interest distributions 2-3 business days after they are received. If you have not received an interest payment on one of your BDN investments, this is because the underlying loan has not made its interest payment. Our team continues to reach out to past due borrowers and work them through our asset management and loss mitigation process.

We continue to strive to provide detailed and timely updates on all individual BDN investments while balancing the time spent on updates relative to focusing that time towards creating positive outcomes. In the last month we’ve posted updates on 59% of outstanding loans. We’re continuing to focus on those that are behind on either payments or maturity date. We’ll continue to strive to provide additional updates on these investments and keep the information updated best we can. Please know that even if an update hasn’t been posted, we’re monitoring and working each loan towards a resolution.

RBNF

There haven’t been any payoffs for loans in which RBNF holds a position in the last month. The balance on RBNF notes is $1.744M. The remaining underlying loans that support this balance are all in later-stage default and being worked on by the asset management team. We continue to work on resolving the underlying loans to create liquidity for distributions on these notes.

Horizon

The Q1 2025 report was recently posted, which you can review here. We continue to see quarter over quarter improvement to returns.

The Fund is currently open and accepting new investments, with the next admittance date scheduled for June 1st, 2025. We’ve begun purchasing new loans into the Fund as we are returning to market on the origination side of our business. We expect performance of the Fund to continue to improve over the coming quarters as new loans are added and delinquent loans are resolved.

General Business Update

The origination side of the business continues to grow month over month. We’re expecting to meet our new business goals for May. We completed a repositioning of our product offerings and are already seeing solid traction. We’ve also implemented two new distribution channels and are seeing positive early results. Again, growing the new loan origination volume is important for the long-term health of the company and is what will provide the operating cashflow to support our ability to continue to execute our plan.

In the coming month, we’ll be focusing on reinvigorating our go-to-market strategy on the capital raising side of our business. We’ll be refreshing the marketing materials and positioning for the Horizon Fund and have some exciting new product enhancements we’ll be announcing as well.

We continue to appreciate your support, understanding and patience as we rebuild the business. We look forward to continuing to serve.

Matt and The Upright Team

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

April 28th, 2025

Dear Investors,

Below is an update as we continue to make progress on our plans to return capital to investors while simultaneously rebuilding our origination capabilities for the long-term success of the Company. We appreciate your continued support and will continue to provide updates here once per month.

PFNF

This week we will be initiating a PFNF principal distribution for $1.4M, which represents ~5.77% of the remaining PFNF note balance. We’ve now returned 67.5% of all PFNF principal since we began this distribution plan. Interest collected on the portfolio this period was $17,350 and has been included in the distribution.

Including the $2.0M distribution we made earlier in the month, this brings the total distribution for this reporting period to $3.4M. Similar to last month, we’re expecting a few more payoffs on the last few days of the month or first week of May. To the extent that we receive a meaningful amount in the coming weeks, we may process another distribution in the early part of May.

The below is a current snapshot of where remaining PFNF funds are allocated relative to last time this was reported.

The overall loan portfolio has been reduced by $3.2M in the last month. We started the period with 22 performing and 72 non-performing loans. We had two loans go from NPL to performing and two performing loans become non-performing. Two performing and four non-performing loans repaid this period. The below tables show the movement of loan counts for the period.

Managing this portfolio and expediting loan repayments remains a high priority. Nearly half of our 20 person team is involved on a daily basis in some form of working these loans towards a resolution.

Please consider the components of this analysis are incredibly dynamic as payoffs, loan sales, servicing advances and various reconciliation efforts are ongoing daily.

Borrower Dependent Notes (BDNs)

In the last month, 11 BDN loans have been repaid, representing $2.67M of principal. To the extent that an underlying loan is making interest payments, we continue to process interest distributions 2-3 business days after they are received. If you have not received an interest payment on one of your BDN investments, this is because the underlying loan has not made its interest payment. Our team continues to reach out to past due borrowers and work them through our asset management and loss mitigation process.

We continue to strive to provide detailed and timely updates on all individual BDN investments while balancing the time spent on updates relative to focusing that time towards creating positive outcomes. In the last month we’ve posted updates on 61% of outstanding loans. We’re continuing to focus on those that are behind on either payments or maturity date. We’ll continue to strive to provide additional updates on these investments and keep the information updated best we can. Please know that even if an update hasn’t been posted, we’re monitoring and working each loan towards a resolution.

RBNF

There haven’t been any payoffs for loans in which RBNF holds a position in the last month. The balance on RBNF notes is $1.744M. The remaining underlying loans that support this balance are all in later-stage default and being worked on by the asset management team. We continue to work on resolving the underlying loans to create liquidity for distributions on these notes.

Horizon

The April 2025 monthly report was recently posted, which you can review here.

The Fund is currently open and accepting new investments, with the next admittance date scheduled for May 1st, 2025. We’ve begun purchasing new loans into the Fund as we are returning to market on the origination side of our business. We expect performance of the Fund to continue to improve over the coming quarters as new loans are added and delinquent loans are resolved.

General Business Update

We continue to make progress on rebuilding our origination activity. We’re on track to meet our new business goal for April. Additionally, we’re making enhancements to our product positioning and beginning to tap into new distribution channels, which we expect to help to contribute to continuing to grow our pipeline. Again, growing the new loan origination volume is important for the long-term health of the company and is what will provide the operating cashflow to support our ability to continue to execute our plan.

We continue to appreciate your support, understanding and patience as we rebuild the business. We look forward to continuing to serve.

-Matt and The Upright Team

PFNF

- Undergoing Payoff Reconciliation: This data point was useful earlier when there was a high volume of payoffs as a result of the bulk loan sales. We’re now able to reconcile and move payoffs to the Settled Cash data point within 1-2 days so we no longer have a need for this category. As you can see from recent reports, this has been $0 for several months now so we’re simply removing it.

- Pending Final Settlement for Loan Sales: Similarly, this one is no longer needed as all loans that were part of the bulk sale have settled. Any remaining PFNF amount is accounted for in the Holdback from Loan Sale receivable as part of the Credit Reserve previously outlined.

- Interest Collected: We’re paying out this balance each month, meaning that it will show $0 each month in the current reporting method. As you may have noticed above, we’ll be reporting the amount of interest collected each period that is part of the distribution.

- Portfolio Count Table: We’re also including a new table that shows the count of loans in each grouping with some details on loans moving in and out.

- Definitions: To streamline the report, we’ve removed the definitions of each line item. These definitions can be found in previous updates as needed.

Borrower Dependent Notes (BDNs)

RBNF

Horizon

General Business Update

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

February 17th, 2025

Dear Investors,