Everywhere you look, there’s the same story — the economy is slowing down. It’s difficult to pinpoint the effect on one specific cause: It could be fears of a recession, the Federal Reserve's efforts to keep inflation in check, volatility in the markets, or a combination of these things.

National Trends

One thing that’s certain is that the inflation rate has been slowing down. In November, it dropped to 7.7% after reaching a high of 9.1% back in June. Moreover, the housing market has been cooling off, too — it's not as hot as it was recently and seems to be returning to more "normal" levels. To gain more context, I've been looking at some demand data from the Mortgage Bankers Association of America, and it’s clear that the 30-year mortgage rate has fallen quite a bit. In October, it was at 7.16%, but by the end of November, it had dropped to 6.49%. That's a pretty significant decline of 67 basis points. I've also noticed that the Mortgage Bankers Association of America's Purchase Index has been rising. In November, it was at 160.5, but now it's at 184 (as of January 27, 2023), which is still below the “normal” range of 200.

On the supply side of things, we can see that the total housing inventory is down 3.4%, and the months of supply are hovering around 3. Overall, it’s reasonable to say that the housing market is cooling slightly, although not drastically. Some of the metrics have fallen outside of normal ranges, but they may begin to recover with the pullback in the inflation rate. That is the key takeaway for me: The heat is leaving the housing market, but all signs point to the recent volatility evening out.

Switching From Macro Trends to Local

(All data is from December 2022, unless otherwise noted).

When it comes to the housing market, we often hear about national trends and statistics (like our previous article, The 2022 Housing Market: A Return to "Normal.") As an organization that solely focuses on residential real estate, we’d like to offer an alternative viewpoint: We believe there's no such thing as a true "national housing market." Each geographic area, city, and even neighborhood has its own unique characteristics and factors that influence its supply and demand, so it's important to look at each market separately.

That's why we wanted to focus on a few Ohio metropolitan markets in this article, specifically Cleveland, Cincinnati, Columbus, and the surrounding areas. While these local markets may be impacted by broader economic trends, they each operate based on their own supply and demand fundamentals. It's fascinating and informative to see how these local markets are performing and what's driving the changes we see so that our customers, both active and passive investors, can make educated, well-informed decisions about their investments.

Demand

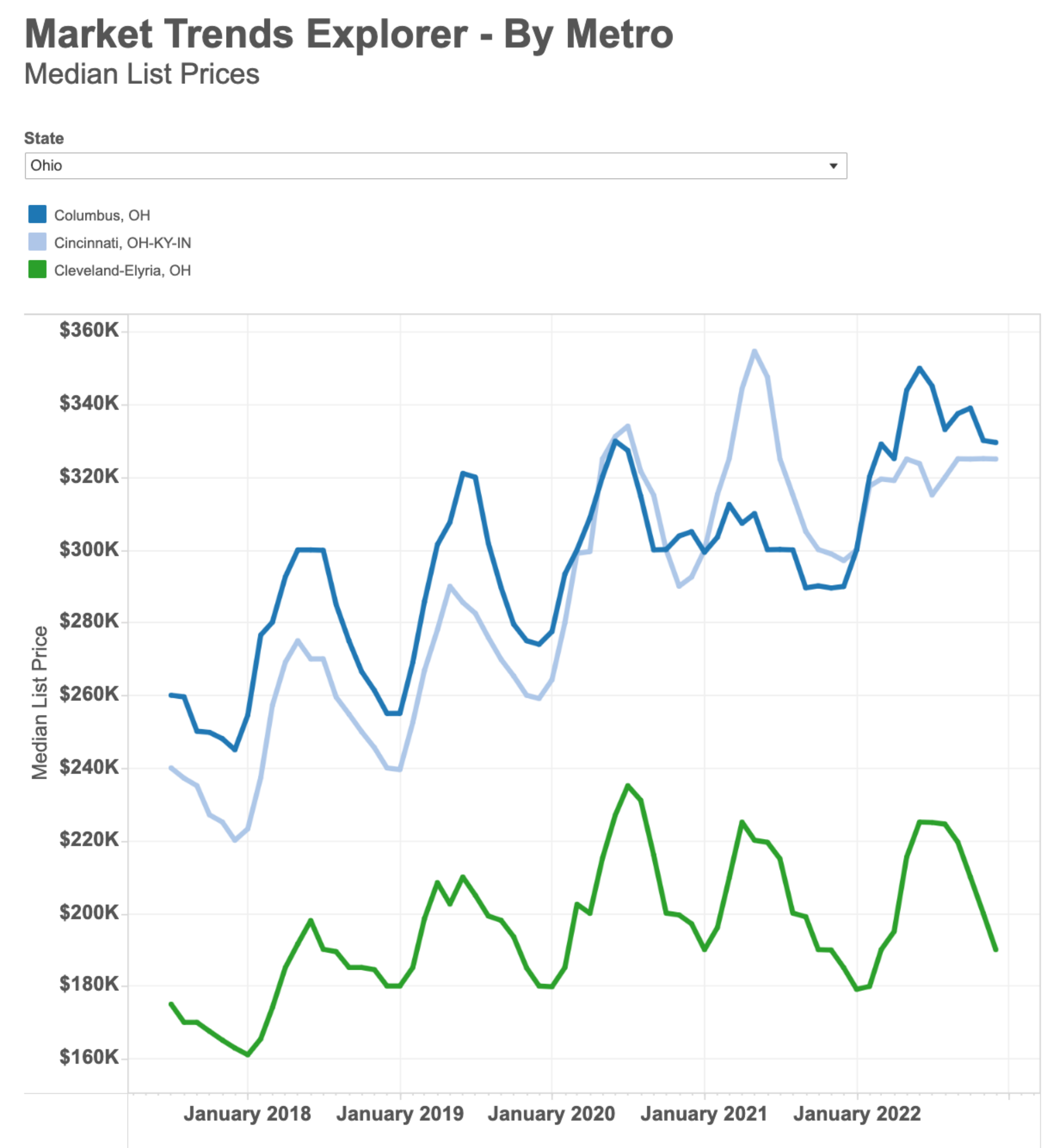

Median List Price

Even though demand for homes is trending toward cooling off, list prices are still rising year-over-year. One reason for this could be that supply is decreasing faster than demand, causing prices to increase. Across Ohio metro areas overall, there has been an 11.4% decrease in the number of homes listed for sale. This could also contribute to the rise in prices, which contrasts the Homes Sold Above List Price and Sales-to-List Price Ratio below.

Median List Prices as of December 2022

- Cleveland, OH

- $190K

- YoY Change: +2.7%

- Columbus, OH

- $329K

- YoY Change: +13.7%

- Cincinnati, OH

- $325K

- YoY Change: 9.4%

Home List Prices

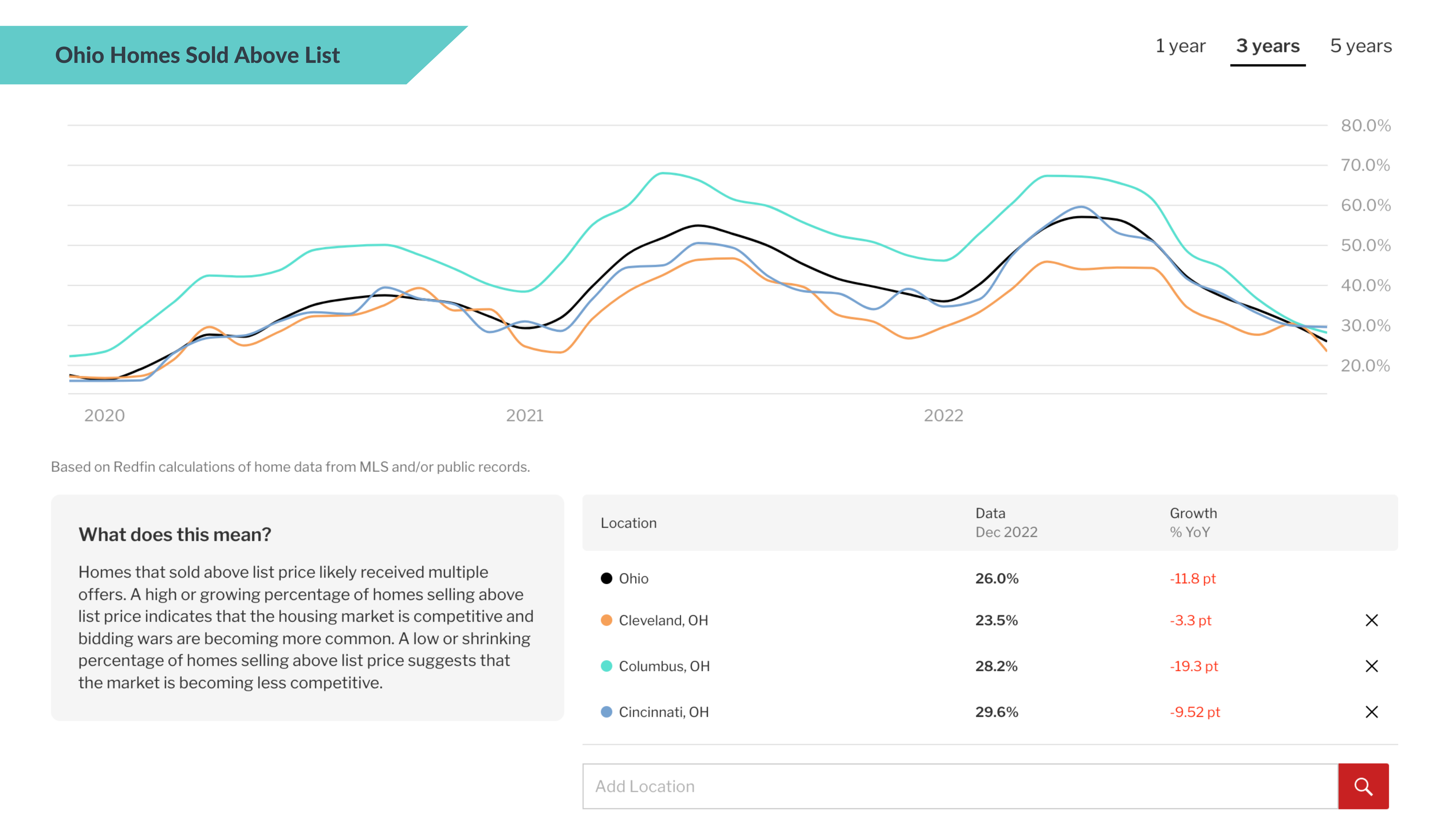

Homes Sold Above List Price Click image to expand.

Click image to expand.

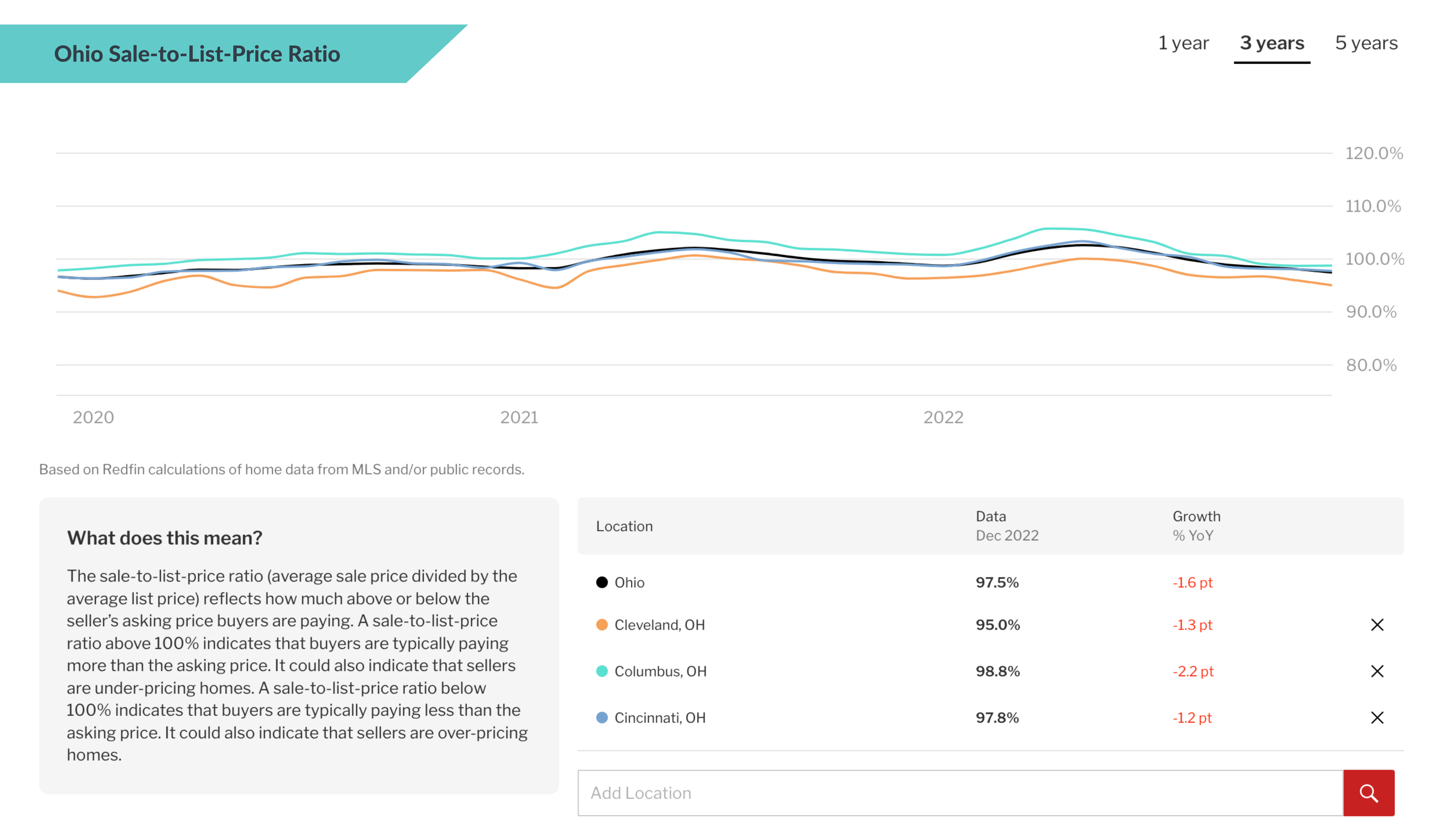

Sale-to-List Price Ratio Click image to expand.

Click image to expand.

There are a few ways to interpret the changes in the housing market metrics we've been discussing. One possibility is that market competitiveness has declined sharply. However, we believe the data supports another viewpoint: We may be returning to pre-pandemic normalcy.

The pandemic caused a rush on housing, leading to a significant increase in pricing and competition. However, as interest rates have risen, many people with 3% interest mortgages have been hesitant to re-enter the market, while others have been priced out of getting a new mortgage. As a result, we've seen a decline in these metrics in recent months. Despite this decline, the percentage of homes sold above the list price is still higher than it was in 2018. Most analysts agree that we would need to see a sustained downward trend below 20% before it becomes newsworthy.

Another metric to consider is the sales-to-list price ratio, which has been abnormally high at above 100%. On a national level, we expect this ratio to hover around 98%. These trends suggest that we may be returning to more normal levels in the housing market.

| December 2018 – Pre | December 2020 – Mid | December 2022 – Post | |

| Cleveland | 96.3% | 98% | 95% |

| Columbus | 97.4% | 100.1% | 98.8% |

| Cincinnati | 95.9% | 98.4% | 97.8% |

*Based on Redfin calculations of home data from MLS and/or public records.

Looking at the pre-, mid-, and post-pandemic levels in Ohio, we see we're getting close the what is considered the normal range of 98%, although Cleveland and Cincinnati are slightly below. While the sold-above-list-price ratio has been on an upward trend over the past few years, the days-on-market metric has seen the opposite.

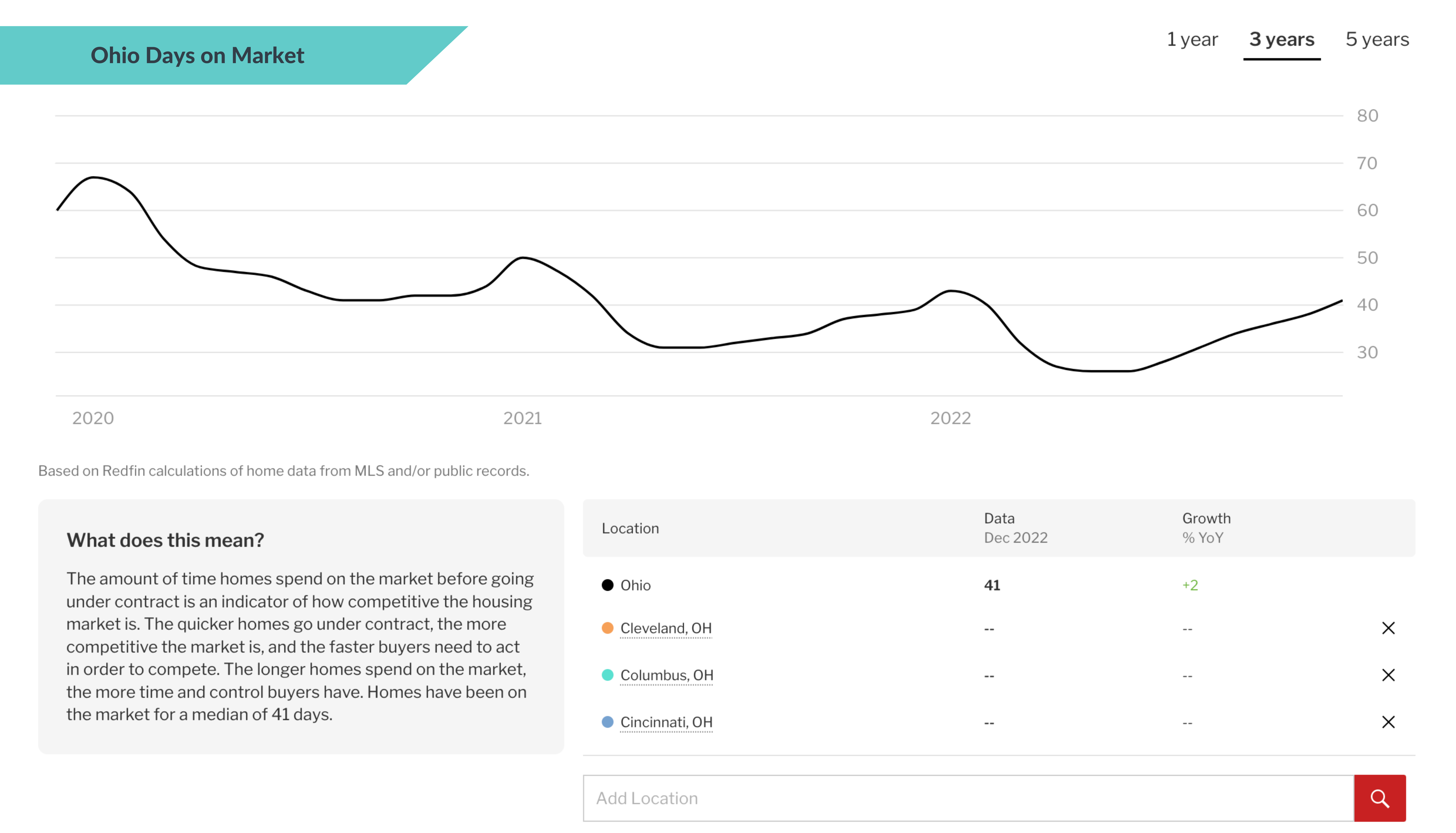

Days On Market

Click image to expand.

Click image to expand.

It's worth noting that, even before the pandemic, the median days on market had been steadily decreasing, with no significant changes to the pattern. This trend is consistent with the overall decline in housing inventory that we've seen, which we'll talk about next.

So, to summarize the key takeaways from the data:

- While there has been a decline in demand, it hasn't been sharp enough to bring us below pre-pandemic levels, yet.

- The supply of homes is decreasing faster than demand, which is helping to support the continued increase in prices.

- Patterns such as the decrease in days on market were already in motion before the pandemic.

Overall, trends point to the housing market is returning to more normal levels, even as demand has cooled off slightly.

Supply

Total Inventory

As we mentioned earlier, the housing supply has been steadily decreasing even before the pandemic. In our previous analysis of the overall housing market, we estimated that there is a shortage of 3-5 million housing units.

| December 2018 – Pre | December 2020 – Mid | December 2022 – Post | |

| Cleveland | 1,663 | 1,300 | 1,531 |

| Columbus | 3,041 | 2,880 | 2,394 |

| Cincinnati | 2,409 | 2,019 | 1,267 |

*Based on Redfin calculations of home data from MLS and/or public records.

There are a few factors contributing to this trend. One is a generally risk-averse environment that has been around since the 2008 housing crisis. Add to that the current interest rate environment, and we see that there is less liquidity from normal sellers who may be hesitant to give up their low 3% interest rates. There are also fewer distressed sellers in the market right now since the majority of mortgage originations in recent years have gone to prime and prime+ borrowers with responsible financial habits.

New construction has also been a factor. Prior to the 2008 crash, we were building well over the average of 1 million homes per year, but construction levels dropped dramatically after the crash and have not yet returned to normal levels. For a more in-depth breakdown of these trends, here's another reminder to check out our article The 2022 Housing Market: A Return to 'Normal.'

Speaking of new construction, let’s dig into months of all housing supply.

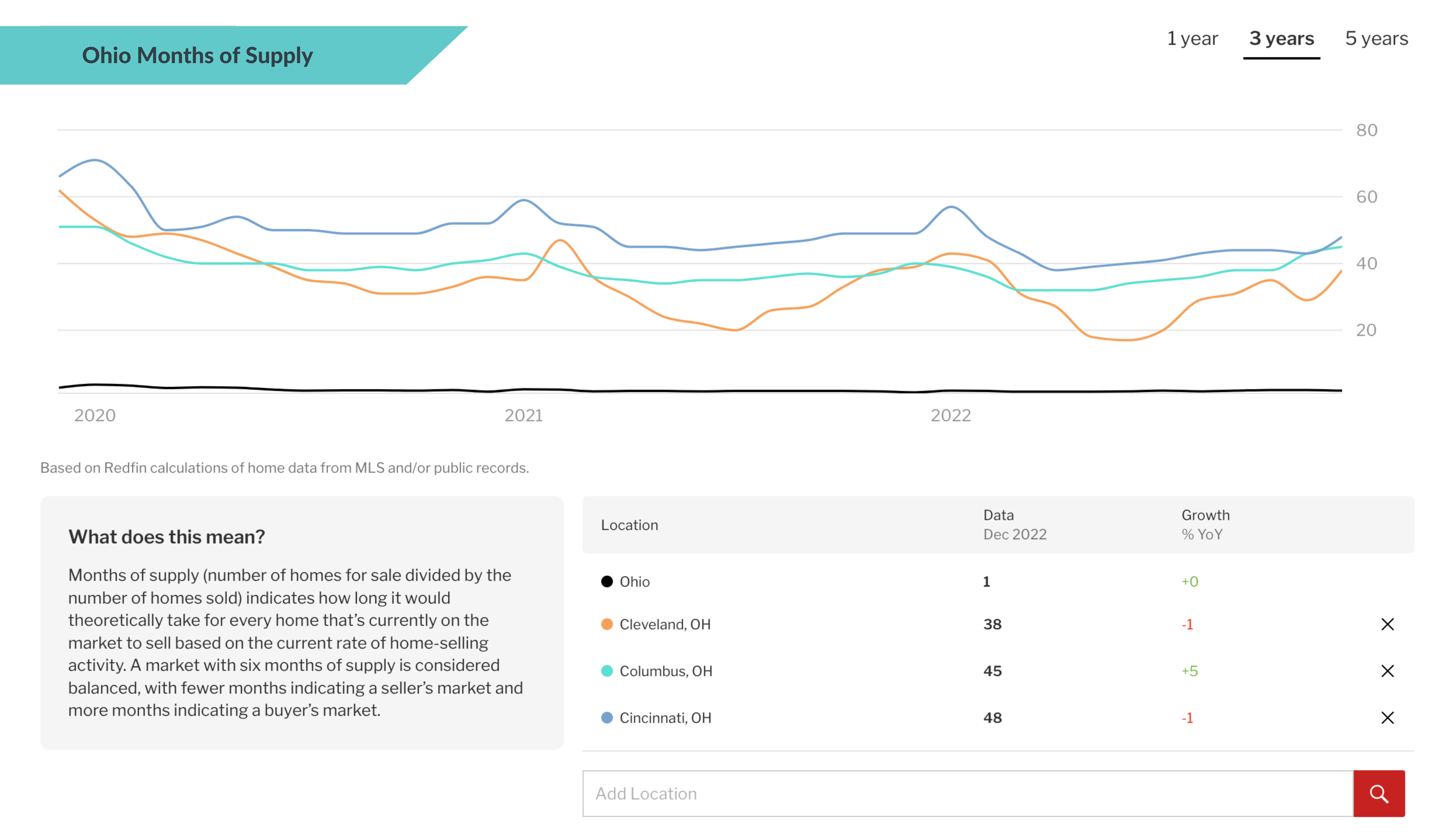

Months of Supply

Click image to expand.

Click image to expand.

In December 2018, the average months of supply for the Cleveland, Columbus, and Cincy metros was about 3 months, and has been trending downward, as seen above, since then. Since early 2022, Ohio supply has been holding steady with about 2 months of supply. Overall, the housing supply has been steadily decreasing since before the pandemic, and this trend is likely to continue driving prices higher until demand starts falling faster than supply. While houses may be sitting on the market longer, they haven't been there long enough to be considered a buyers' market.

To summarize:

- Housing supply has been steadily decreasing, which will continue to push prices higher until demand starts falling faster than supply.

- Houses are sitting on the market longer but not for long enough for it to be considered a buyers' market.

What to Look For

It looks like demand for housing in Ohio has softened — almost to a "normal" range. However, the low supply is still keeping prices high. While we don't believe the current downward trend is cause for immediate concern, there are a few things to watch out for as potential indicators of a slowing market:

- List prices are a key indicator of demand. If prices suddenly shift to a sustained downward trend without an increase in supply, it could be a sign of a weakening market. Similarly, if the percentage of homes sold above list price drops below 15% for a sustained period, this could be newsworthy.

- Something else to pay attention to is the sales-to-list-price ratio. If this falls below pre-pandemic levels, it could indicate that we've entered a buyers' market.

- Finally, while the days on market have been steadily decreasing, it would be worth noting if there was a long-term shift in the other direction.

- It looks like the supply of housing in Ohio is continuing to decrease, unlike the national market. While this might not be new information, it's worth keeping an eye on a few key metrics to see if any changes are on the horizon.

- The changes in total housing inventory could have multiple effects. If builders start to pull back going into the new year to see what the interest rate environment looks like, it could impact new construction activity. Even if things look good, getting new construction projects off the ground will probably take some time.

- The last metric is months of supply. Houses are currently taking longer to sell, but if mortgage rates start to decline, we could see an increase in demand. If that happens, it will be interesting to see if houses start selling faster again.

Overall, the Ohio market still has plenty of opportunity for successful investing, with the potential for strong returns despite a slightly higher risk. It's worth noting that the Ohio market has underlying supply factors that didn't change during the pandemic, and the changes in demand we saw were abnormal spikes in key metrics. The opportunity lies in the gap between these abnormal spikes and the pre-existing patterns, which we’ll continue to monitor here at Fund That Flip.

Interested in investing in Ohio real estate and earning up to 13.5% returns? Check out some of our current opportunities.

Disclaimer: Projects funded and principal repaid are reflective of Fund That Flip's overall platform performance and are not necessarily indicative of the returns of any specific investment product offered.

Past performance is not indicative of future performance. Investors should not rely on forward-looking statements because such statements are inherently uncertain and involve risks. No returns are guaranteed and these types of investments involve a high degree of risk.

Neither the Securities and Exchange Commission nor any federal or state securities commission or any other regulatory authority has recommended or approved of the investment or the accuracy or inaccuracy of any of the information or materials provided by or through the website. Direct and indirect purchase of real estate property involves significant risks, including, but not limited to risk related to sale of land, market and industry risks and risks specific to a given property. Investments are not bank deposits, are not insured by the FDIC or by any other Federal Government Agency, are not guaranteed by Fund That Flip, Inc., and may lose value.

Fund That Flip, Inc. does not make investment recommendations, and this message should not be construed as such. This message is not an offer to sell or the solicitation of an offer to buy any security, which can only be made through official offering documents that contain important information about risks, fees and expenses. Any investment information contained herein has been secured from sources Fund That Flip, Inc. believes are reliable, but we make no representations or warranties as to the accuracy of such information and accept no liability therefor. We recommend that you consult with a financial advisor, attorney, accountant, and any other professional that can help you to understand and assess the risks associated with any investment opportunity. If and when Fund That Flip, Inc. is able to make investment opportunities available, only accredited investors who submit required verification will be able to invest.

Graphics and data from Realtor.com and Redfin.

Ready to get a fix and flip loan? Check out our Hard Money Lender team in Ohio or Click below to get started: